The relationship between overextended personal debt and credit score damage is a profound and destructive feedback loop, each fueling the other in a c...

Read More

The crisis of overextended personal debt is a complex financial state where liabilities become unmanageable, and its profound impact on an individual�...

Read More

The phenomenon of overextended personal debt is not merely a financial condition but a complex web of interconnected core concepts that trap individua...

Read More

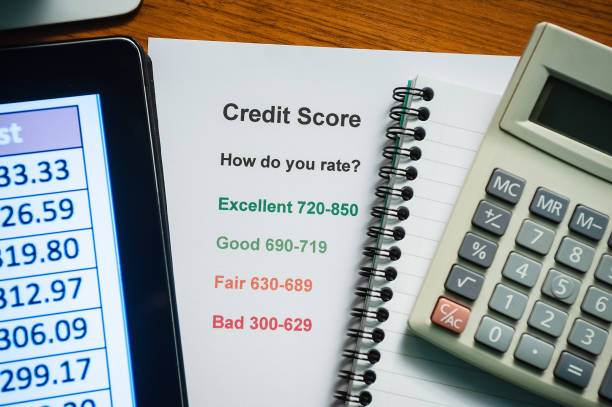

In the realm of personal finance, few concepts are as crucial yet as commonly conflated as the credit report and the credit score. While the terms are...

Read More

The short answer is that enrolling in a formal hardship program can impact your credit score, but the nature of that impact is nuanced and often less ...

Read More

The weight of managing multiple debts can feel overwhelming, leading many to consider debt consolidation as a path to simplicity and financial control...

Read MoreBase your budget on your lowest expected monthly income. During higher-income months, allocate the extra funds directly to debt repayment or your emergency fund. This conservative approach prevents overspending.

Key fees include late payment fees, over-the-limit fees, and foreign transaction fees. Understanding these penalties is essential to avoid unexpected costs that add to your debt burden.

Nonprofit credit counselors, patient advocacy groups, and legal aid organizations can help negotiate bills, navigate financial assistance, and address collections issues.

No, but the path to recovery is long. Negative information typically remains on your credit report for 7 years. Rebuilding requires consistent, on-time payments, reducing balances, and demonstrating responsible financial behavior over time to restore your credit health and financial stability.

This is the tendency to continue a behavior because of previously invested resources. Someone might continue pouring money into a failing business to justify past investments, going deeper into debt rather than cutting their losses, because they feel they've "come too far to quit."