For most middle-class households, a utility bill is just another monthly expense that arrives like clockwork. You pay the electric company, the gas provider, the water utility, and the internet service provider without thinking too much about it. These are not luxury items. They are the basic infrastructure of daily life. But when money gets tight, these same bills often become the first payments that get skipped. The reasoning makes sense on the surface. You figure the electric company will send a reminder. The water utility will tack on a late fee. Eventually, you will catch up. What many people do not realize is that unpaid utility and service debt can do serious damage to your credit score, sometimes in ways that feel completely unfair.The problem starts with how utility companies handle nonpayment. For decades, most utility providers did not report your payment history to the major credit bureaus at all. They would send your account to a collection agency after several months of missed payments, and that collection account would appear on your credit report. That collection hit could drop your score by a hundred points or more. Today, the landscape has shifted. More than a dozen major utility companies now report your payment activity to at least one of the three credit bureaus every single month. This means a single overdue water bill can show up on your credit report as a negative mark, not just when it goes to collections, but while you are still in the process of trying to get current.The real trap for middle-class consumers is the lag between the missed payment and the credit report update. You might think you have a thirty-day grace period. That is often true for late fees. But for credit reporting purposes, a payment that is thirty days past due can already be on your report. Even if you pay the full amount on day thirty-one, the damage is done. The credit bureaus keep a record of that thirty-day delinquency. It stays on your report for seven years. One late payment on an $85 water bill can make your car loan or credit card application more expensive for the better part of a decade.Utility debt is also dangerous because it tends to pile up quietly. A missed electric bill in July might lead to a higher bill in August because you are now paying for the previous usage plus the current usage plus late fees. Before you know it, you owe four hundred dollars instead of one hundred. That is the moment when many middle-class families decide to pay the minimum on their credit card and let the utility bill slide another month. They do not realize they are setting themselves up for a utility shutoff, and in many states, a shutoff can result in a reconnection fee that gets added to the balance. Suddenly, a manageable debt has become a crisis.There is also a less obvious form of utility and service debt that catches people off guard. This is the debt tied to automatic payments and banking errors. If you have an internet bill set to auto-pay, and your checking account balance runs low, the payment might bounce. The internet company charges a returned payment fee. Your bank charges an overdraft fee. The internet company does not get paid. Thirty days later, you have a delinquency on your credit report. You did not make a choice to skip the payment. You simply forgot to check your balance. The result is the same.For middle-class consumers who are already stretched thin, the best protection against utility debt is a simple one. You need to give these bills priority treatment. That means paying your electricity, water, gas, and internet before you pay your streaming subscriptions, your dining out, or even your credit card minimum. It feels counterintuitive because credit cards are the financial product that appears on your credit report most directly. But a utility delinquency can be just as damaging, and the consequences of a shutoff are immediate and stressful. You cannot work from home without internet. You cannot cook or shower without water and gas.If you are already behind on a utility bill, take action immediately. Call the company and ask about a payment arrangement. Most utility providers are required by state law to offer you some form of extended payment plan, especially if you can demonstrate financial hardship. Ask them explicitly whether they report late payments to the credit bureaus. Some companies will agree to hold off on reporting if you make a good faith effort to catch up. This is not guaranteed, but it never hurts to ask. The worst they can say is no.One other strategy worth noting is the use of a prepaid debit card or a separate checking account specifically for utility bills. If you know that your main checking account is often near zero, diverting the utility payment to a separate account that only receives your utility money can prevent the overdraft scenario. It adds a layer of friction that forces you to be intentional about whether you can afford a given month’s payment.Ultimately, the key to managing utility and service debt is to stop thinking of these bills as flexible. They are not. They are as important as your rent or mortgage for the purposes of your credit health. Treating a water bill with the same seriousness as a car payment is the only way to avoid the quiet, creeping damage that these small debts can cause.

For most middle-class households, a utility bill is just another monthly expense that arrives like clockwork. You pay the electric company, the gas provider, the water utility, and the internet service provider without thinking too much about it. These are not luxury items. They are the basic infrastructure of daily life. But when money gets tight, these same bills often become the first payments that get skipped. The reasoning makes sense on the surface. You figure the electric company will send a reminder. The water utility will tack on a late fee. Eventually, you will catch up. What many people do not realize is that unpaid utility and service debt can do serious damage to your credit score, sometimes in ways that feel completely unfair.The problem starts with how utility companies handle nonpayment. For decades, most utility providers did not report your payment history to the major credit bureaus at all. They would send your account to a collection agency after several months of missed payments, and that collection account would appear on your credit report. That collection hit could drop your score by a hundred points or more. Today, the landscape has shifted. More than a dozen major utility companies now report your payment activity to at least one of the three credit bureaus every single month. This means a single overdue water bill can show up on your credit report as a negative mark, not just when it goes to collections, but while you are still in the process of trying to get current.The real trap for middle-class consumers is the lag between the missed payment and the credit report update. You might think you have a thirty-day grace period. That is often true for late fees. But for credit reporting purposes, a payment that is thirty days past due can already be on your report. Even if you pay the full amount on day thirty-one, the damage is done. The credit bureaus keep a record of that thirty-day delinquency. It stays on your report for seven years. One late payment on an $85 water bill can make your car loan or credit card application more expensive for the better part of a decade.Utility debt is also dangerous because it tends to pile up quietly. A missed electric bill in July might lead to a higher bill in August because you are now paying for the previous usage plus the current usage plus late fees. Before you know it, you owe four hundred dollars instead of one hundred. That is the moment when many middle-class families decide to pay the minimum on their credit card and let the utility bill slide another month. They do not realize they are setting themselves up for a utility shutoff, and in many states, a shutoff can result in a reconnection fee that gets added to the balance. Suddenly, a manageable debt has become a crisis.There is also a less obvious form of utility and service debt that catches people off guard. This is the debt tied to automatic payments and banking errors. If you have an internet bill set to auto-pay, and your checking account balance runs low, the payment might bounce. The internet company charges a returned payment fee. Your bank charges an overdraft fee. The internet company does not get paid. Thirty days later, you have a delinquency on your credit report. You did not make a choice to skip the payment. You simply forgot to check your balance. The result is the same.For middle-class consumers who are already stretched thin, the best protection against utility debt is a simple one. You need to give these bills priority treatment. That means paying your electricity, water, gas, and internet before you pay your streaming subscriptions, your dining out, or even your credit card minimum. It feels counterintuitive because credit cards are the financial product that appears on your credit report most directly. But a utility delinquency can be just as damaging, and the consequences of a shutoff are immediate and stressful. You cannot work from home without internet. You cannot cook or shower without water and gas.If you are already behind on a utility bill, take action immediately. Call the company and ask about a payment arrangement. Most utility providers are required by state law to offer you some form of extended payment plan, especially if you can demonstrate financial hardship. Ask them explicitly whether they report late payments to the credit bureaus. Some companies will agree to hold off on reporting if you make a good faith effort to catch up. This is not guaranteed, but it never hurts to ask. The worst they can say is no.One other strategy worth noting is the use of a prepaid debit card or a separate checking account specifically for utility bills. If you know that your main checking account is often near zero, diverting the utility payment to a separate account that only receives your utility money can prevent the overdraft scenario. It adds a layer of friction that forces you to be intentional about whether you can afford a given month’s payment.Ultimately, the key to managing utility and service debt is to stop thinking of these bills as flexible. They are not. They are as important as your rent or mortgage for the purposes of your credit health. Treating a water bill with the same seriousness as a car payment is the only way to avoid the quiet, creeping damage that these small debts can cause.

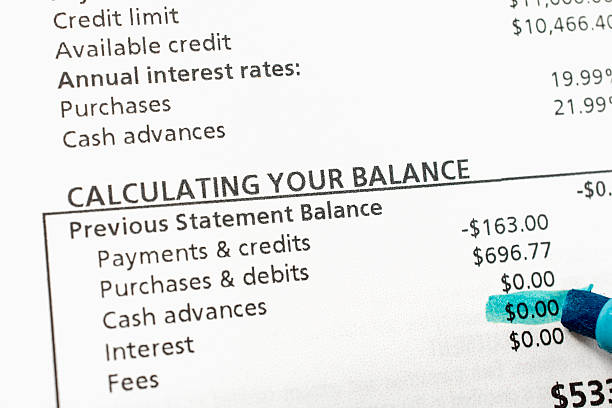

The Annual Percentage Rate (APR) is critical, as it determines the cost of carrying a balance. A lower APR means more of your payment goes toward the principal debt, not interest.

A high PTI leaves little room for error. When an unexpected expense arises, you may be forced to use high-interest credit cards or payday loans to cover it, which adds a new minimum payment and drives your PTI even higher, deepening the cycle of debt.

Providers may require a security deposit or deny service altogether if you have a history of non-payment with them or other utilities.

Compound interest is interest calculated on the initial principal and on the accumulated interest from previous periods. For a saver, it's powerful; for a debtor, it's dangerous. It causes debt to grow exponentially if only minimum payments are made, making it much harder to pay off.

Almost never. Withdrawing funds from a 401(k) early comes with massive penalties (10%) and income taxes, erasing a huge chunk of your savings. You also lose the future compound growth on that money. This should be considered an absolute last resort.