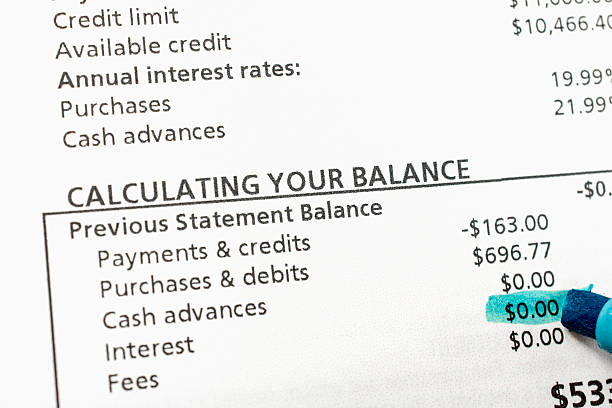

For many, credit cards are a convenient financial tool, but the ease of spending can lead to a persistent and costly problem: carrying a high balance from month to month. This common practice does not merely accrue interest charges; it actively and significantly harms your credit score, a critical number that influences your ability to secure loans, rent apartments, and even obtain certain jobs. The impact primarily revolves around a key metric known as your credit utilization ratio, a factor that can cause swift and substantial fluctuations in your score.At the heart of the issue is the credit utilization ratio, which is the amount of revolving credit you are using compared to your total available limits. This ratio is calculated both per individual card and across all your cards in aggregate. Credit scoring models, most notably FICO and VantageScore, heavily weigh this factor, often accounting for approximately 30% of your score, making it the second most important component after payment history. The fundamental rule is simple: a lower ratio is better. Financial experts consistently recommend keeping your overall utilization below 30%, with the highest scores typically going to those who maintain a ratio in the single digits. When you carry a high balance, you push this ratio upward, signaling to lenders that you may be overextended, financially strained, and a higher-risk borrower. This perceived risk directly translates into a lower credit score.The damage manifests in several interconnected ways. First, a high utilization rate triggers an almost immediate drop in your score. Unlike other factors that have a longer history, utilization is a snapshot of your debt at the time your credit card issuer reports to the bureaus, usually once per billing cycle. This means that even if you pay off the balance in full every month, if your payment is recorded after the reporting date, the bureaus will still see the high balance, and your score will suffer temporarily. Secondly, consistently high balances suggest a reliance on credit to fund your lifestyle, which can be a red flag during manual loan reviews, even if your score has managed to stay afloat due to other positive behaviors. Furthermore, carrying high balances can limit your ability to improve other areas of your credit profile. For instance, applying for a new card to increase your total available credit and thus lower your utilization ratio might result in a denial due to the very balances you are trying to mitigate.Beyond the direct hit to your utilization, there are secondary consequences. The high-interest charges that accompany carried balances can strain your monthly budget, making it more challenging to pay all your bills on time. A single missed payment, which severely damages your payment history, could then compound the initial problem. Additionally, if your high balances persist, credit card companies may become hesitant to grant you credit limit increases, or in some cases, they might even decrease your existing limits. Such an action would cause your utilization ratio to spike even further, creating a frustrating cycle of credit score decline. It is also worth noting that while paying down high balances is the solution, the recovery is not always instantaneous. Positive payment history builds over time, and while your score can rebound quickly once you lower your utilization, the memory of high balances can linger in the eyes of some lenders.Ultimately, carrying a high credit card balance is a double financial penalty: you pay substantial interest to your lender while simultaneously undermining your own financial reputation. Your credit score is a reflection of responsible credit management, and high utilization tells a story of potential distress. By prioritizing paying down these balances and aiming to pay your statement in full each month, you do more than save money on interest; you actively build and protect the credit score that will unlock better financial opportunities and terms for your future. The path to a strong credit score is paved with low balances, consistent payments, and a clear demonstration that you are in control of your credit, not the other way around.

For many, credit cards are a convenient financial tool, but the ease of spending can lead to a persistent and costly problem: carrying a high balance from month to month. This common practice does not merely accrue interest charges; it actively and significantly harms your credit score, a critical number that influences your ability to secure loans, rent apartments, and even obtain certain jobs. The impact primarily revolves around a key metric known as your credit utilization ratio, a factor that can cause swift and substantial fluctuations in your score.At the heart of the issue is the credit utilization ratio, which is the amount of revolving credit you are using compared to your total available limits. This ratio is calculated both per individual card and across all your cards in aggregate. Credit scoring models, most notably FICO and VantageScore, heavily weigh this factor, often accounting for approximately 30% of your score, making it the second most important component after payment history. The fundamental rule is simple: a lower ratio is better. Financial experts consistently recommend keeping your overall utilization below 30%, with the highest scores typically going to those who maintain a ratio in the single digits. When you carry a high balance, you push this ratio upward, signaling to lenders that you may be overextended, financially strained, and a higher-risk borrower. This perceived risk directly translates into a lower credit score.The damage manifests in several interconnected ways. First, a high utilization rate triggers an almost immediate drop in your score. Unlike other factors that have a longer history, utilization is a snapshot of your debt at the time your credit card issuer reports to the bureaus, usually once per billing cycle. This means that even if you pay off the balance in full every month, if your payment is recorded after the reporting date, the bureaus will still see the high balance, and your score will suffer temporarily. Secondly, consistently high balances suggest a reliance on credit to fund your lifestyle, which can be a red flag during manual loan reviews, even if your score has managed to stay afloat due to other positive behaviors. Furthermore, carrying high balances can limit your ability to improve other areas of your credit profile. For instance, applying for a new card to increase your total available credit and thus lower your utilization ratio might result in a denial due to the very balances you are trying to mitigate.Beyond the direct hit to your utilization, there are secondary consequences. The high-interest charges that accompany carried balances can strain your monthly budget, making it more challenging to pay all your bills on time. A single missed payment, which severely damages your payment history, could then compound the initial problem. Additionally, if your high balances persist, credit card companies may become hesitant to grant you credit limit increases, or in some cases, they might even decrease your existing limits. Such an action would cause your utilization ratio to spike even further, creating a frustrating cycle of credit score decline. It is also worth noting that while paying down high balances is the solution, the recovery is not always instantaneous. Positive payment history builds over time, and while your score can rebound quickly once you lower your utilization, the memory of high balances can linger in the eyes of some lenders.Ultimately, carrying a high credit card balance is a double financial penalty: you pay substantial interest to your lender while simultaneously undermining your own financial reputation. Your credit score is a reflection of responsible credit management, and high utilization tells a story of potential distress. By prioritizing paying down these balances and aiming to pay your statement in full each month, you do more than save money on interest; you actively build and protect the credit score that will unlock better financial opportunities and terms for your future. The path to a strong credit score is paved with low balances, consistent payments, and a clear demonstration that you are in control of your credit, not the other way around.

Review reports from all three bureaus at least annually (via AnnualCreditReport.com). During debt repayment, monitor every 3-6 months to track progress and dispute errors.

This is a negotiation where you offer to pay the debt in exchange for the collector completely removing the negative entry from your credit report. While not all collectors agree to this, it is the best possible outcome for your credit health.

Bankruptcy is a last resort but may be a necessary legal tool if your debt is so overwhelming that there is no realistic mathematical possibility of paying it off within 5 years, even with drastic budget cuts and increased income.

When income drops abruptly, but fixed expenses and debt payments remain the same, a previously manageable financial situation can quickly become unsustainable. This forces individuals to rely on credit or fall behind on payments, leading to overextension.

Monthly reviews are ideal. Update for changes in income, expenses, or debt goals. Regular check-ins keep you accountable and allow for timely adjustments.