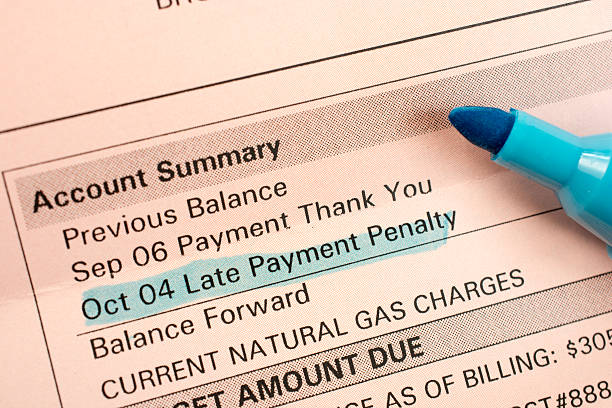

Your credit report is a detailed summary of your borrowing history. It shows every loan, credit card, and payment account you have had in the past seven to ten years. Lenders, landlords, and even some employers use this report to decide whether you are financially responsible. If you do not check it regularly, you might miss mistakes or signs of fraud that could cost you money or block you from getting a mortgage or car loan. Reviewing your credit report is one of the simplest prevention strategies you can use to protect your financial health. But you have to know what you are actually looking for when you open that file.The first area to check is your personal information. This includes your name, current and past addresses, Social Security number, and date of birth. Look for any misspellings or outdated addresses. Sometimes a minor error like a wrong middle initial can cause confusion, but more important is whether a name or address appears that you do not recognize. That could mean someone else’s information got mixed into your report, or worse, that an identity thief is using your personal details. If you see an address in a city you have never lived in, that is a red flag that needs immediate investigation.Next, move to the section that lists your accounts. This is where you will see every credit card, mortgage, auto loan, student loan, or other line of credit tied to your name. For each account, check the account number, the date it was opened, the credit limit or loan amount, and the current balance. Make sure the status is correct. For example, a closed account should show “closed” or “paid in full,” not “open.” A late payment that you know you paid on time should not appear. Even one wrong late payment mark can drop your credit score by dozens of points. Look at the dates of the last activity. If an old account shows recent activity that you did not do, that could be a sign someone else is using a credit line you forgot about.After accounts, review the inquiries section. Inquiries are records of who has looked at your credit report. There are two types: hard inquiries and soft inquiries. Hard inquiries happen when you apply for credit, and they can slightly lower your score. Soft inquiries happen when you check your own report or when a company pre-approves you for offers. You should only see hard inquiries that you authorized. If you spot a hard inquiry from a lender you never applied to, that is a strong warning sign of identity theft. Someone may have attempted to open an account in your name. You have the right to dispute any unauthorized inquiry.Next, check the public records section. This part lists bankruptcies, tax liens, or civil judgments. Most of these items are rare for the typical middle-class consumer, but if you see a bankruptcy or a judgment that is not yours, it can be devastating. Even a single mistake here could prevent you from renting an apartment or getting a loan. Make sure any public record matches your personal situation and that the dates are accurate. Also confirm that the record has been removed after the legal time limit, usually seven to ten years, because some bureaus fail to update automatically.Finally, look at the collections accounts. If you have ever had a medical bill or a utility bill go unpaid, it might have been sent to a collection agency. Sometimes these collections are sold to multiple agencies, and the same debt gets reported more than once. You might also see a collection for a debt you already paid. Each collection account damages your credit score, so it is in your interest to catch duplicates or paid-off debts that should have been removed. If the collection is older than seven years from the original delinquency, it should no longer appear.Beyond checking for errors and fraud, reviewing your report helps you understand your overall credit health. You can see which accounts are helping your score by having long histories and low balances, and which accounts might be dragging you down because of high utilization or missed payments. This knowledge lets you make smarter decisions about which credit cards to keep open and which debts to pay off first. For example, if you see a credit card with a balance that is near its limit, paying that down will likely boost your score more than paying a smaller balance on a card that is only 20 percent utilized.The law gives you one free credit report every twelve months from each of the three major credit bureaus—Equifax, Experian, and TransUnion. You can request them all at once or space them out throughout the year. Many people choose to check one bureau every four months so they have a rolling view of their credit. There are also paid monitoring services, but the free reports are enough for most middle-class consumers if you take the time to review them carefully.Make it a habit to set aside thirty minutes once a year to go through your report with a fine-tooth comb. Keep a list of any discrepancies you find, and use the official dispute process on each bureau’s website to correct them. The bureaus are required by law to investigate your dispute within 30 days. A clean, accurate credit report is one of your best financial tools. It costs you nothing but time, and it can save you thousands of dollars in higher interest rates or lost opportunities.

Your credit report is a detailed summary of your borrowing history. It shows every loan, credit card, and payment account you have had in the past seven to ten years. Lenders, landlords, and even some employers use this report to decide whether you are financially responsible. If you do not check it regularly, you might miss mistakes or signs of fraud that could cost you money or block you from getting a mortgage or car loan. Reviewing your credit report is one of the simplest prevention strategies you can use to protect your financial health. But you have to know what you are actually looking for when you open that file.The first area to check is your personal information. This includes your name, current and past addresses, Social Security number, and date of birth. Look for any misspellings or outdated addresses. Sometimes a minor error like a wrong middle initial can cause confusion, but more important is whether a name or address appears that you do not recognize. That could mean someone else’s information got mixed into your report, or worse, that an identity thief is using your personal details. If you see an address in a city you have never lived in, that is a red flag that needs immediate investigation.Next, move to the section that lists your accounts. This is where you will see every credit card, mortgage, auto loan, student loan, or other line of credit tied to your name. For each account, check the account number, the date it was opened, the credit limit or loan amount, and the current balance. Make sure the status is correct. For example, a closed account should show “closed” or “paid in full,” not “open.” A late payment that you know you paid on time should not appear. Even one wrong late payment mark can drop your credit score by dozens of points. Look at the dates of the last activity. If an old account shows recent activity that you did not do, that could be a sign someone else is using a credit line you forgot about.After accounts, review the inquiries section. Inquiries are records of who has looked at your credit report. There are two types: hard inquiries and soft inquiries. Hard inquiries happen when you apply for credit, and they can slightly lower your score. Soft inquiries happen when you check your own report or when a company pre-approves you for offers. You should only see hard inquiries that you authorized. If you spot a hard inquiry from a lender you never applied to, that is a strong warning sign of identity theft. Someone may have attempted to open an account in your name. You have the right to dispute any unauthorized inquiry.Next, check the public records section. This part lists bankruptcies, tax liens, or civil judgments. Most of these items are rare for the typical middle-class consumer, but if you see a bankruptcy or a judgment that is not yours, it can be devastating. Even a single mistake here could prevent you from renting an apartment or getting a loan. Make sure any public record matches your personal situation and that the dates are accurate. Also confirm that the record has been removed after the legal time limit, usually seven to ten years, because some bureaus fail to update automatically.Finally, look at the collections accounts. If you have ever had a medical bill or a utility bill go unpaid, it might have been sent to a collection agency. Sometimes these collections are sold to multiple agencies, and the same debt gets reported more than once. You might also see a collection for a debt you already paid. Each collection account damages your credit score, so it is in your interest to catch duplicates or paid-off debts that should have been removed. If the collection is older than seven years from the original delinquency, it should no longer appear.Beyond checking for errors and fraud, reviewing your report helps you understand your overall credit health. You can see which accounts are helping your score by having long histories and low balances, and which accounts might be dragging you down because of high utilization or missed payments. This knowledge lets you make smarter decisions about which credit cards to keep open and which debts to pay off first. For example, if you see a credit card with a balance that is near its limit, paying that down will likely boost your score more than paying a smaller balance on a card that is only 20 percent utilized.The law gives you one free credit report every twelve months from each of the three major credit bureaus—Equifax, Experian, and TransUnion. You can request them all at once or space them out throughout the year. Many people choose to check one bureau every four months so they have a rolling view of their credit. There are also paid monitoring services, but the free reports are enough for most middle-class consumers if you take the time to review them carefully.Make it a habit to set aside thirty minutes once a year to go through your report with a fine-tooth comb. Keep a list of any discrepancies you find, and use the official dispute process on each bureau’s website to correct them. The bureaus are required by law to investigate your dispute within 30 days. A clean, accurate credit report is one of your best financial tools. It costs you nothing but time, and it can save you thousands of dollars in higher interest rates or lost opportunities.

Your 40s are peak earning years and your last major window to build retirement wealth. Debt payments directly sabotage your ability to save, jeopardizing your entire retirement plan and leaving insufficient time to recover.

The most immediate consequence is intense financial stress and anxiety. The constant pressure of managing payments and the fear of missing them creates a persistent state of worry that affects mental and physical well-being.

Set up automatic payments for at least the minimum amount due on all your accounts. This is the most reliable method to avoid accidental missed payments due to forgetfulness or a busy schedule.

Non-profit organizations like the National Foundation for Credit Counseling (NFCC) offer certified financial counselors. For mental health, consider therapy, community health services, or support groups like Debtors Anonymous. The 988 Suicide & Crisis Lifeline is available for immediate crisis support.

A credit limit is the maximum amount you can borrow on a revolving account. Exceeding this limit typically results in fees and can damage your credit score. A lower limit can also force a high credit utilization ratio, which hurts your score.