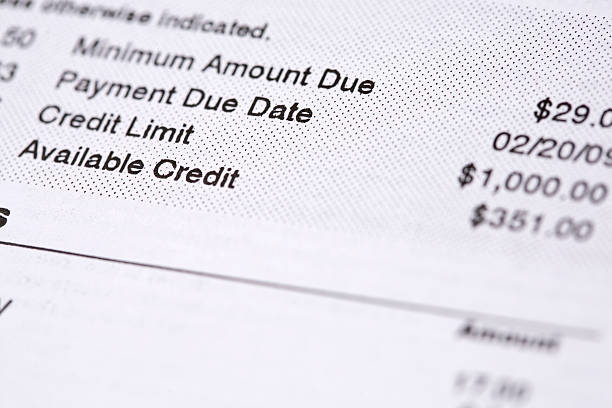

If you have been using credit cards for a while, you have probably heard the term debt-to-limit ratio. It sounds complicated, but it is actually a simple idea. It is the amount of money you owe on your credit cards divided by the total amount of credit you have available. If you have a card with a five thousand dollar limit and you owe one thousand dollars, your debt-to-limit ratio is twenty percent. Lenders look at this number to decide if you are a risky borrower. The lower your ratio, the better your credit score usually is.Many middle-class consumers focus on paying down their balances to improve this ratio. That is a good strategy. But there is another way to lower your ratio that many people overlook. You can ask for a credit limit increase. When you get approved for a higher limit, the amount you owe stays the same, but your available credit goes up. That means your debt-to-limit ratio drops immediately. It is a simple math trick that can give your credit score a quick boost without you having to spend a single extra dollar on your bills.The key is to understand when and how to ask. Not every request is a good idea. If you have a history of missed payments or high balances, a lender might say no. That can be a problem because some lenders do a hard inquiry on your credit report when you ask for a limit increase. A hard inquiry can temporarily lower your score by a few points. So you want to make sure you are in good shape before you ask. Check your credit score first. If it is above seven hundred, you have a decent chance. If it is lower, focus on paying down debt first.You also need to consider your income. Lenders will want to know that you can handle more credit. If you have a steady job and you have not changed jobs recently, that helps your case. Be honest about your income on the request form. Do not inflate it. Lenders can verify this information, and lying can get your account closed.Another thing to watch out for is the temptation to spend more. When you get a higher limit, it can feel like free money. But it is not. If you run up your balance again, your debt-to-limit ratio will go right back up. Worse, you could end up in a cycle where you keep asking for increases and then maxing out the card. That is the opposite of what you want. The goal is to keep your balance low or pay it off in full every month. A higher limit is a tool for improving your credit health, not a license to spend.There is also the matter of timing. If you have a big purchase coming up, like a car or a house, do not ask for a limit increase in the months before you apply for the loan. Even a small hard inquiry can ding your score, and you need every point you can get for a mortgage or auto loan. Ask for the increase at least six months before you plan to apply for major credit. That gives your score time to recover and for the new limit to be reported to the credit bureaus.Some people worry that having too much available credit will make them look risky to lenders. That is a myth. Unless you are actually using that credit, having a high total limit is almost always a good thing. It shows that other lenders trust you, and it lowers your overall debt-to-limit ratio. Lenders love to see a ratio under thirty percent. If you can get it under ten percent, that is even better.One more thing to keep in mind. Not all credit cards are the same. Some issuers are generous with limit increases. Others are stingy. If you have a card from a major bank that you have used responsibly for a year or more, you have a good shot. For newer cards, wait at least six months before asking. And do not ask too often. Once every six to twelve months is plenty. Too many requests in a short period can make you look desperate for credit, which is a red flag.In the end, a credit limit increase is a straightforward way to improve your debt-to-limit ratio without needing extra cash. It works best when you combine it with good habits like paying on time and keeping your spending under control. If you use it wisely, it can help your credit score climb over time. And a better score means lower interest rates, better loan terms, and more financial flexibility for you and your family.

If you have been using credit cards for a while, you have probably heard the term debt-to-limit ratio. It sounds complicated, but it is actually a simple idea. It is the amount of money you owe on your credit cards divided by the total amount of credit you have available. If you have a card with a five thousand dollar limit and you owe one thousand dollars, your debt-to-limit ratio is twenty percent. Lenders look at this number to decide if you are a risky borrower. The lower your ratio, the better your credit score usually is.Many middle-class consumers focus on paying down their balances to improve this ratio. That is a good strategy. But there is another way to lower your ratio that many people overlook. You can ask for a credit limit increase. When you get approved for a higher limit, the amount you owe stays the same, but your available credit goes up. That means your debt-to-limit ratio drops immediately. It is a simple math trick that can give your credit score a quick boost without you having to spend a single extra dollar on your bills.The key is to understand when and how to ask. Not every request is a good idea. If you have a history of missed payments or high balances, a lender might say no. That can be a problem because some lenders do a hard inquiry on your credit report when you ask for a limit increase. A hard inquiry can temporarily lower your score by a few points. So you want to make sure you are in good shape before you ask. Check your credit score first. If it is above seven hundred, you have a decent chance. If it is lower, focus on paying down debt first.You also need to consider your income. Lenders will want to know that you can handle more credit. If you have a steady job and you have not changed jobs recently, that helps your case. Be honest about your income on the request form. Do not inflate it. Lenders can verify this information, and lying can get your account closed.Another thing to watch out for is the temptation to spend more. When you get a higher limit, it can feel like free money. But it is not. If you run up your balance again, your debt-to-limit ratio will go right back up. Worse, you could end up in a cycle where you keep asking for increases and then maxing out the card. That is the opposite of what you want. The goal is to keep your balance low or pay it off in full every month. A higher limit is a tool for improving your credit health, not a license to spend.There is also the matter of timing. If you have a big purchase coming up, like a car or a house, do not ask for a limit increase in the months before you apply for the loan. Even a small hard inquiry can ding your score, and you need every point you can get for a mortgage or auto loan. Ask for the increase at least six months before you plan to apply for major credit. That gives your score time to recover and for the new limit to be reported to the credit bureaus.Some people worry that having too much available credit will make them look risky to lenders. That is a myth. Unless you are actually using that credit, having a high total limit is almost always a good thing. It shows that other lenders trust you, and it lowers your overall debt-to-limit ratio. Lenders love to see a ratio under thirty percent. If you can get it under ten percent, that is even better.One more thing to keep in mind. Not all credit cards are the same. Some issuers are generous with limit increases. Others are stingy. If you have a card from a major bank that you have used responsibly for a year or more, you have a good shot. For newer cards, wait at least six months before asking. And do not ask too often. Once every six to twelve months is plenty. Too many requests in a short period can make you look desperate for credit, which is a red flag.In the end, a credit limit increase is a straightforward way to improve your debt-to-limit ratio without needing extra cash. It works best when you combine it with good habits like paying on time and keeping your spending under control. If you use it wisely, it can help your credit score climb over time. And a better score means lower interest rates, better loan terms, and more financial flexibility for you and your family.

Calculate your Debt-to-Income (DTI) ratio. If your total monthly debt payments divided by your gross monthly income is above 36-40%, you are likely overextended. Also, a Payment-to-Income (PTI) ratio above 20% is a strong cash-flow warning sign.

High minimum payments act as a mandatory financial leash. They consume cash flow that could otherwise be directed to savings, investments, or discretionary spending, forcing you into a reactive financial position instead of a proactive one.

The Debt Snowball method (paying smallest balances first) provides psychological wins that boost motivation. The Debt Avalanche method (paying highest interest rates first) saves the most money on interest. Choose the strategy that best fits your personality and will keep you consistent.

Your self-worth is not defined by your net worth. Financial difficulties are a life circumstance, not a character flaw. Practicing self-compassion is essential for maintaining the mental strength needed to navigate the path to financial recovery.

Yes, but providers typically require multiple notices and must follow state regulations. Shut-offs are often a last resort, especially for essential services like electricity or water.