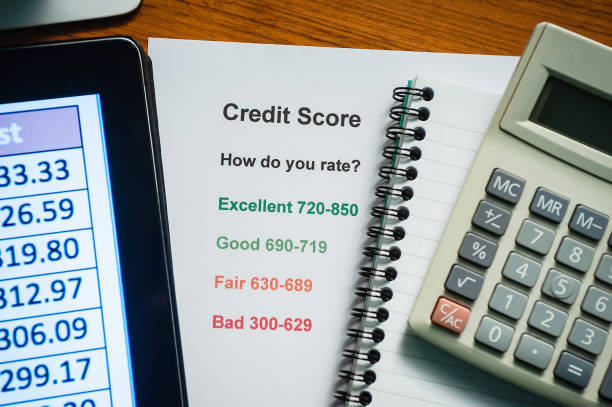

Your credit score is a numerical representation of your financial trustworthiness, a key that can unlock favorable interest rates or slam doors on financial opportunities. While responsibly managed debt, such as a mortgage or student loan, can actually build a positive credit history, excessive or poorly managed debt is one of the most significant factors that can damage your score. The damage occurs through several interconnected mechanisms within the FICO and VantageScore calculation models, each reflecting a heightened risk to potential lenders.The most immediate and substantial impact comes from your credit utilization ratio, which accounts for approximately 30% of your FICO score. This ratio measures the amount of revolving credit you are using compared to your total available limits. For instance, if you have a total credit card limit of $10,000 and carry a $9,000 balance, your utilization is a very high 90%. Credit scoring models interpret high utilization as a sign of financial strain and over-reliance on credit. The general rule of thumb is to keep your overall utilization below 30%, with the best scores going to those who maintain it in the single digits. High balances from carrying debt directly inflate this ratio, signaling to lenders that you may be struggling to manage your finances, thereby lowering your score.Beyond overall utilization, the sheer amount of debt you hold affects your score through your credit mix and new credit inquiries, which together make up about 10% and 10% of your score, respectively. An over-reliance on high-interest credit card debt, as opposed to a healthy mix of installment and revolving loans, can be viewed negatively. Furthermore, if debt leads you to seek additional credit cards or personal loans to manage cash flow, each application typically triggers a hard inquiry. While a single inquiry might only cause a minor dip, several in a short period compound the damage and paint a picture of desperation to lenders, further eroding your score.Perhaps the most severe damage, however, stems from payment history, the single most important factor at 35% of your score. When debt becomes unmanageable, the risk of missing a payment—even by just 30 days—increases dramatically. A single late payment can be reported to the credit bureaus and remain on your credit report for seven years, causing a significant and lasting drop in your score. As debt spirals, consistent late payments, accounts sent to collections, or worst of all, bankruptcy or foreclosure, create deep and long-lasting scars on your credit report. These derogatory marks are red flags to future lenders and can take years of diligent financial behavior to overcome.Finally, high levels of existing debt can negatively impact your debt-to-income ratio (DTI), which is not directly part of your credit score but is critically examined by lenders during any application process. A high DTI suggests that a large portion of your income is already committed to debt repayment, leaving you less able to handle new obligations. This can lead to loan denials, which, while not hurting your score directly, limit your financial options and can force you into less favorable credit arrangements if you do secure them.In essence, debt damages your credit score by creating a cascade of negative indicators within the scoring algorithms. It raises your credit utilization, increases the risk of missed payments, may lead to a flurry of hard inquiries, and can ultimately result in severe derogatory marks. The score is designed to predict risk, and high, unmanageable debt is a clear predictor of potential default. Therefore, managing debt prudently—keeping balances low, making payments consistently on time, and avoiding overextension—is not merely good financial practice but is fundamental to building and maintaining a strong credit score, which in turn paves the way for a more secure financial future.

Your credit score is a numerical representation of your financial trustworthiness, a key that can unlock favorable interest rates or slam doors on financial opportunities. While responsibly managed debt, such as a mortgage or student loan, can actually build a positive credit history, excessive or poorly managed debt is one of the most significant factors that can damage your score. The damage occurs through several interconnected mechanisms within the FICO and VantageScore calculation models, each reflecting a heightened risk to potential lenders.The most immediate and substantial impact comes from your credit utilization ratio, which accounts for approximately 30% of your FICO score. This ratio measures the amount of revolving credit you are using compared to your total available limits. For instance, if you have a total credit card limit of $10,000 and carry a $9,000 balance, your utilization is a very high 90%. Credit scoring models interpret high utilization as a sign of financial strain and over-reliance on credit. The general rule of thumb is to keep your overall utilization below 30%, with the best scores going to those who maintain it in the single digits. High balances from carrying debt directly inflate this ratio, signaling to lenders that you may be struggling to manage your finances, thereby lowering your score.Beyond overall utilization, the sheer amount of debt you hold affects your score through your credit mix and new credit inquiries, which together make up about 10% and 10% of your score, respectively. An over-reliance on high-interest credit card debt, as opposed to a healthy mix of installment and revolving loans, can be viewed negatively. Furthermore, if debt leads you to seek additional credit cards or personal loans to manage cash flow, each application typically triggers a hard inquiry. While a single inquiry might only cause a minor dip, several in a short period compound the damage and paint a picture of desperation to lenders, further eroding your score.Perhaps the most severe damage, however, stems from payment history, the single most important factor at 35% of your score. When debt becomes unmanageable, the risk of missing a payment—even by just 30 days—increases dramatically. A single late payment can be reported to the credit bureaus and remain on your credit report for seven years, causing a significant and lasting drop in your score. As debt spirals, consistent late payments, accounts sent to collections, or worst of all, bankruptcy or foreclosure, create deep and long-lasting scars on your credit report. These derogatory marks are red flags to future lenders and can take years of diligent financial behavior to overcome.Finally, high levels of existing debt can negatively impact your debt-to-income ratio (DTI), which is not directly part of your credit score but is critically examined by lenders during any application process. A high DTI suggests that a large portion of your income is already committed to debt repayment, leaving you less able to handle new obligations. This can lead to loan denials, which, while not hurting your score directly, limit your financial options and can force you into less favorable credit arrangements if you do secure them.In essence, debt damages your credit score by creating a cascade of negative indicators within the scoring algorithms. It raises your credit utilization, increases the risk of missed payments, may lead to a flurry of hard inquiries, and can ultimately result in severe derogatory marks. The score is designed to predict risk, and high, unmanageable debt is a clear predictor of potential default. Therefore, managing debt prudently—keeping balances low, making payments consistently on time, and avoiding overextension—is not merely good financial practice but is fundamental to building and maintaining a strong credit score, which in turn paves the way for a more secure financial future.

The most common examples are mortgages (secured by the house) and auto loans (secured by the vehicle). Other examples can include secured credit cards (backed by a cash deposit), and some personal loans that use a savings account or certificate of deposit as collateral.

Most hospitals and providers offer interest-free installment plans. Always ask about this option before using credit cards or loans.

Absolutely. A good credit score reflects past payment history, but a high PTI is a forward-looking indicator of risk. It shows you are vulnerable to any financial disruption, like a job loss or unexpected expense, which could quickly lead to missed payments and debt default.

Yes, if you have the time and energy. A side gig can provide dedicated "debt destruction" money without forcing you to cut your regular budget to the bone. Use all or most of the earnings from your side hustle specifically for extra debt payments.

Create sinking funds—set aside a small amount monthly for predictable irregular expenses. This prevents reliance on credit when costs arise.