The phenomenon of overextended personal debt is not merely a financial condition but a complex web of interconnected core concepts that trap individua...

Read More

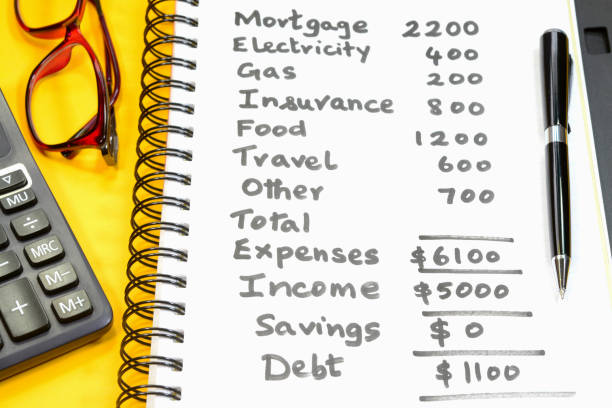

The personal budget, in its most ideal form, is a blueprint for financial freedom, a tool for aligning dreams with dollars. Yet, for an individual gra...

Read More

The journey into overextended personal debt often begins with a breakdown in personal budgeting, and the path out is almost invariably paved with its ...

Read More

Conscious spending is a transformative financial philosophy that moves beyond mere budgeting to cultivate a deliberate and values-aligned relationship...

Read More

In an age of curated perfection and instant gratification, financial stability is increasingly undermined by two subtle yet powerful forces: lifestyle...

Read More

In an era defined by readily available credit and complex financial products, the specter of debt overextension looms large for many. While numerous s...

Read MoreWhile scores above 670 are considered "good," focus on steady improvement. Moving from a "Poor" score (below 580) to a "Fair" score (580-669) is a significant first milestone that opens up more options.

Yes, scoring models look at both your overall utilization across all cards and the utilization on each individual account. Maxing out a single card, even if others have low balances, can still hurt your score.

Debt consolidation involves taking out a new loan (often at a lower rate) to pay off multiple existing debts, simplifying payments. Debt settlement involves negotiating with creditors to pay a lump sum that is less than the full amount owed, which severely damages your credit.

A debt consolidation loan can be framed as "saving $100 a month" (a gain) or "paying $5,000 in interest" (a loss). We are more risk-averse when a choice is framed in terms of losses. Lenders often use gain-framing to make consolidation appealing, downplaying the total long-term cost.

This is a state law that sets a time limit on how long a creditor or collector can sue you to collect a debt. The time period varies by state and debt type, but making a partial payment can sometimes restart the clock.