The concept of strategic credit application may seem counterintuitive for someone grappling with overextended personal debt, yet it represents a sophi...

Read More

The journey to repair a credit report while actively repaying debt can feel like navigating a labyrinth. It requires a dual focus: methodically addres...

Read More

In the complex landscape of personal finance, the act of comparing credit cards for existing debt is far more than a simple administrative task; it is...

Read More

In the bustling marketplace of modern business, time is the ultimate currency. For sales professionals, recruiters, and service providers alike, the s...

Read More

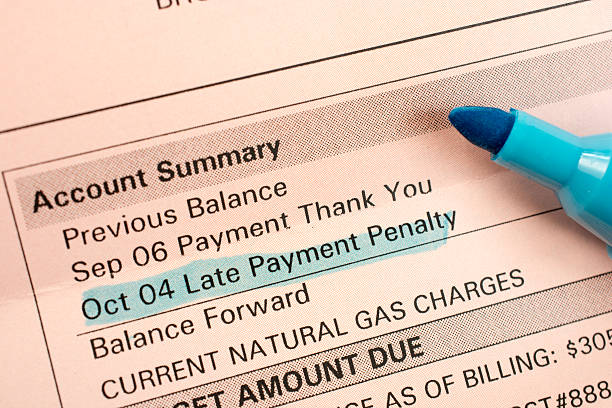

The weight of multiple debts can feel paralyzing, leaving many unsure where to even begin the journey toward financial freedom. The question of which ...

Read More

In the complex ecosystem of modern finance, a credit application is often perceived as a simple transactional document—a formality required to acces...

Read MoreEven a small emergency fund ($500-$1,000) prevents unexpected expenses from derailing your budget and forcing you deeper into debt. It should be a fixed category in your budget until funded.

Conspicuous consumption is the public acquisition and display of luxury goods or services primarily to signal wealth, status, or social standing, rather than to meet essential needs.

The Debt Snowball method (paying smallest balances first) provides psychological wins that boost motivation. The Debt Avalanche method (paying highest interest rates first) saves the most money on interest. Choose the strategy that best fits your personality and will keep you consistent.

Lifestyle inflation, also known as lifestyle creep, is the tendency to increase your spending as your income rises. Instead of saving or investing the extra money, it gets absorbed into a more expensive lifestyle, leaving your savings rate stagnant and making you more vulnerable to debt.

Financial problems are a leading cause of arguments and stress in marriages and partnerships. Disagreements over spending, secrecy about debt, and the constant pressure can erode trust and lead to separation or divorce.