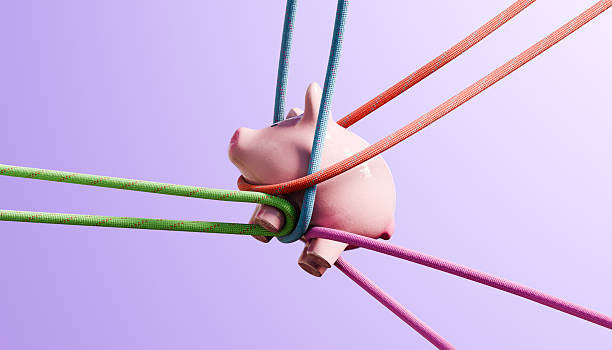

The specter of debt looms over individuals, corporations, and nations alike, a tool for growth that can swiftly transform into a trap. While the long-term consequences of excessive borrowing are well-documented—stagnant growth, eroded creditworthiness, intergenerational burdens—the most immediate and visceral consequence is a severe liquidity crisis. This acute cash flow shortage acts as a domino, toppling financial stability and forcing drastic, often painful, corrective actions. The immediate fallout of overextended debt is not a distant bankruptcy filing or a theoretical economic collapse; it is the palpable, daily struggle to meet obligations when income can no longer cover outflows.When an entity is overextended, its financial structure becomes perilously rigid. Every available dollar of revenue is pre-allocated to service debt—covering minimum payments on credit cards, loans, and bonds. This leaves no buffer for unexpected expenses, economic downturns, or even routine fluctuations in income. The first and most pressing symptom is the scramble to prioritize payments. Essential costs like payroll for a business, or rent and groceries for an individual, must now compete with mandatory debt servicing. This creates impossible choices: pay the electricity bill or the credit card minimum? Fund inventory or the bank loan? This triage mentality consumes mental energy and operational focus, diverting resources from productive activity toward financial survival.This liquidity squeeze rapidly escalates into a cascade of punitive financial events. Missed payments trigger late fees and penalty interest rates, which contractually skyrocket, making the existing debt burden even heavier. For example, a credit card’s annual percentage rate may jump from 15% to 30% after a single missed payment, mathematically accelerating the debt spiral. Simultaneously, credit scores and credit ratings plummet. For an individual, this means access to new lines of credit—even for emergencies—vanishes. For a company, its commercial paper may become unsellable, and suppliers may demand cash-on-delivery, further strangling operations. The entity finds itself locked out of the very financial systems it needs to navigate the crisis.The psychological and operational impact is equally immediate and debilitating. Decision-making becomes reactive and short-term. A business may fire essential staff, liquidate assets at fire-sale prices, or cancel crucial investments in maintenance and research, sacrificing its future viability for present survival. An individual may resort to predatory payday loans or drain retirement accounts, incurring taxes and penalties, to keep creditors at bay. The constant stress of financial jeopardy impairs judgment, clouds strategic thinking, and can lead to a paralysis where no positive action seems possible. The overextended entity is not planning for growth; it is operating in a state of financial distress, where every day is a challenge to stave off collapse.Ultimately, this combination of cash shortage, punitive financial penalties, and constrained options forces a drastic reckoning. The immediate consequence culminates in the necessity for a sudden and often brutal adjustment. This may take the form of debt restructuring, where creditors are forced to negotiate terms, often at a loss. It could mean asset forfeiture, such as a home foreclosure or car repossession. For a nation, it could mean imposing austerity measures—sharp cuts to public services and pensions—that spark social unrest. In the worst cases, it leads to formal bankruptcy or default, a legal admission of failure that carries long-lasting scars. These are not gradual transitions but breaking points, arrived at when the liquidity well runs completely dry.Therefore, while the seeds of overextension are sown over time through accumulated borrowing, the harvest is a sudden and acute financial heart attack. The most immediate consequence is not the final insolvency itself, but the debilitating liquidity crisis that precedes it—a period of intense pressure where cash vanishes, options narrow, and survival becomes a daily calculation. It is a stark reminder that debt’s true cost is measured not just in interest paid, but in the loss of flexibility, security, and the capacity to withstand the ordinary uncertainties of economic life. The first domino to fall is always liquidity, and once it tips, the chain reaction toward crisis is difficult to stop.

The specter of debt looms over individuals, corporations, and nations alike, a tool for growth that can swiftly transform into a trap. While the long-term consequences of excessive borrowing are well-documented—stagnant growth, eroded creditworthiness, intergenerational burdens—the most immediate and visceral consequence is a severe liquidity crisis. This acute cash flow shortage acts as a domino, toppling financial stability and forcing drastic, often painful, corrective actions. The immediate fallout of overextended debt is not a distant bankruptcy filing or a theoretical economic collapse; it is the palpable, daily struggle to meet obligations when income can no longer cover outflows.When an entity is overextended, its financial structure becomes perilously rigid. Every available dollar of revenue is pre-allocated to service debt—covering minimum payments on credit cards, loans, and bonds. This leaves no buffer for unexpected expenses, economic downturns, or even routine fluctuations in income. The first and most pressing symptom is the scramble to prioritize payments. Essential costs like payroll for a business, or rent and groceries for an individual, must now compete with mandatory debt servicing. This creates impossible choices: pay the electricity bill or the credit card minimum? Fund inventory or the bank loan? This triage mentality consumes mental energy and operational focus, diverting resources from productive activity toward financial survival.This liquidity squeeze rapidly escalates into a cascade of punitive financial events. Missed payments trigger late fees and penalty interest rates, which contractually skyrocket, making the existing debt burden even heavier. For example, a credit card’s annual percentage rate may jump from 15% to 30% after a single missed payment, mathematically accelerating the debt spiral. Simultaneously, credit scores and credit ratings plummet. For an individual, this means access to new lines of credit—even for emergencies—vanishes. For a company, its commercial paper may become unsellable, and suppliers may demand cash-on-delivery, further strangling operations. The entity finds itself locked out of the very financial systems it needs to navigate the crisis.The psychological and operational impact is equally immediate and debilitating. Decision-making becomes reactive and short-term. A business may fire essential staff, liquidate assets at fire-sale prices, or cancel crucial investments in maintenance and research, sacrificing its future viability for present survival. An individual may resort to predatory payday loans or drain retirement accounts, incurring taxes and penalties, to keep creditors at bay. The constant stress of financial jeopardy impairs judgment, clouds strategic thinking, and can lead to a paralysis where no positive action seems possible. The overextended entity is not planning for growth; it is operating in a state of financial distress, where every day is a challenge to stave off collapse.Ultimately, this combination of cash shortage, punitive financial penalties, and constrained options forces a drastic reckoning. The immediate consequence culminates in the necessity for a sudden and often brutal adjustment. This may take the form of debt restructuring, where creditors are forced to negotiate terms, often at a loss. It could mean asset forfeiture, such as a home foreclosure or car repossession. For a nation, it could mean imposing austerity measures—sharp cuts to public services and pensions—that spark social unrest. In the worst cases, it leads to formal bankruptcy or default, a legal admission of failure that carries long-lasting scars. These are not gradual transitions but breaking points, arrived at when the liquidity well runs completely dry.Therefore, while the seeds of overextension are sown over time through accumulated borrowing, the harvest is a sudden and acute financial heart attack. The most immediate consequence is not the final insolvency itself, but the debilitating liquidity crisis that precedes it—a period of intense pressure where cash vanishes, options narrow, and survival becomes a daily calculation. It is a stark reminder that debt’s true cost is measured not just in interest paid, but in the loss of flexibility, security, and the capacity to withstand the ordinary uncertainties of economic life. The first domino to fall is always liquidity, and once it tips, the chain reaction toward crisis is difficult to stop.

This is a coping mechanism where an individual ignores bills, avoids answering calls, and refuses to open bank statements. While providing short-term relief from anxiety, it allows late fees and interest to accumulate and problems to escalate, ultimately increasing long-term stress.

It leads to a hollow victory: the temporary thrill of ownership is replaced by lasting financial strain, damaged credit, and missed life opportunities, ultimately undermining the very status and security the spending was meant to project.

Get a full financial picture. Gather all your statements and list every debt—credit cards, student loans, car loans, etc. For each, note the total balance, interest rate (APR), and minimum monthly payment. You can't make a plan until you know exactly what you're dealing with.

Debt becomes intertwined with major life expenses like a mortgage, costs of raising young children, and potentially higher auto loans. The pressure to save for retirement and children's education increases while disposable income may shrink.

Yes, return policies are governed by the retailer, not the BNPL provider. Once the retailer processes your return, they will notify the BNPL company, who will cancel the remaining payments. Note that it can take a billing cycle or two for the refund to be fully processed.