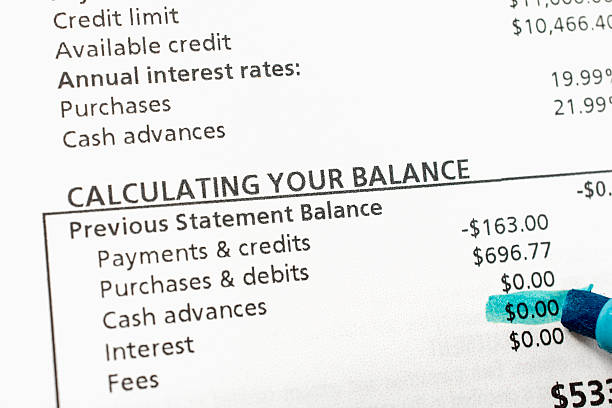

Missing a credit card payment by just one day does not seem like a big deal. You probably figure you will pay it tomorrow or just pay the late fee and move on. But that single slip-up can set off a chain reaction that costs you thousands of dollars and creates months of financial stress. For the middle-class consumer, a late payment is rarely an isolated event. It is often the first domino in a row that eventually topples your entire budget.When you miss a payment, the credit card company immediately hits you with a late fee. On most major cards, that fee can be up to forty-one dollars for the first offense and higher for subsequent ones. That alone stings for a family on a tight budget. But the real damage is what happens next. Your credit card company will look at your account and decide you are now a higher risk. That means your interest rate can skyrocket under what is called the penalty annual percentage rate. Many cards will jump from a standard rate of around eighteen percent all the way up to twenty-nine or thirty percent. That rate applies to your entire balance, not just the past-due amount.Now imagine you carry a balance of five thousand dollars. At eighteen percent, you were paying about seventy-five dollars a month in interest. After the penalty rate kicks in, you are suddenly paying over one hundred and twenty dollars a month in interest alone. That extra forty-five dollars might not sound catastrophic, but it adds up to over five hundred dollars a year in pure waste. That is money that could have gone toward groceries, a car payment, or a small emergency fund. Instead, it is flowing directly to the credit card company just because you paid a bill a few days late.The stress does not end with the rate hike. Your credit score takes a hit the moment that late payment is reported to the credit bureaus. A single thirty-day late payment can drop a good credit score by fifty to one hundred points. For a middle-class consumer, that drop can have immediate real-world consequences. If you need to refinance your car loan or apply for a mortgage, a lower score means a higher interest rate. Over the life of a thirty-year mortgage, a one-percentage-point difference in your rate can cost you tens of thousands of dollars. That is a massive hidden tax you pay simply because you forgot to hit the submit button one time.Once your score drops, other dominoes start to fall. Your auto insurance company may raise your premiums because they use credit-based insurance scores to set rates. Your landlord might decide not to renew your lease or require a larger security deposit. You might lose access to the best credit cards with rewards and cash back, forcing you to rely on less favorable products. Each of these consequences adds another layer of financial pressure to your monthly budget.The mental toll is just as heavy. You start dreading the mail. You avoid checking your bank balance. You argue with your spouse about who forgot to pay the bill. The anxiety bleeds into other areas of your life. You find yourself lying awake at night running numbers in your head, trying to figure out how you will cover the next payment. This kind of chronic financial stress is linked to higher rates of depression, insomnia, and even physical health problems like high blood pressure. It strains marriages and makes it harder to focus at work, which can lead to missed opportunities for raises or promotions.For many middle-class families, the late payment is not a sign of irresponsibility. It is a symptom of playing tug of war with too many bills at once. You are juggling a mortgage, a car payment, student loans, childcare costs, and everyday expenses. Something slips through the cracks, and one late payment spirals into a hole that takes months to climb out of. The irony is that the credit card company offers you a way out by letting you pay over time, but the penalty rates and fees make that process much more expensive and stressful than it needs to be.The best way to avoid this entire cascade is to set up automatic payments for at least the minimum amount due on every account. If you are worried about overdraft fees, you can schedule the payment for a day or two after your paycheck hits. You can also set up text or email alerts for upcoming due dates. These simple steps cost nothing and can prevent the domino effect that turns a simple mistake into a long-term financial headache. One late payment is never just one late payment. It is the beginning of a chain that tightens the financial stress around your household until you break it.

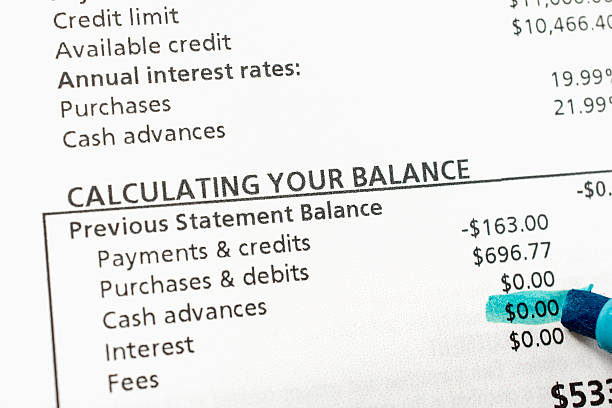

Missing a credit card payment by just one day does not seem like a big deal. You probably figure you will pay it tomorrow or just pay the late fee and move on. But that single slip-up can set off a chain reaction that costs you thousands of dollars and creates months of financial stress. For the middle-class consumer, a late payment is rarely an isolated event. It is often the first domino in a row that eventually topples your entire budget.When you miss a payment, the credit card company immediately hits you with a late fee. On most major cards, that fee can be up to forty-one dollars for the first offense and higher for subsequent ones. That alone stings for a family on a tight budget. But the real damage is what happens next. Your credit card company will look at your account and decide you are now a higher risk. That means your interest rate can skyrocket under what is called the penalty annual percentage rate. Many cards will jump from a standard rate of around eighteen percent all the way up to twenty-nine or thirty percent. That rate applies to your entire balance, not just the past-due amount.Now imagine you carry a balance of five thousand dollars. At eighteen percent, you were paying about seventy-five dollars a month in interest. After the penalty rate kicks in, you are suddenly paying over one hundred and twenty dollars a month in interest alone. That extra forty-five dollars might not sound catastrophic, but it adds up to over five hundred dollars a year in pure waste. That is money that could have gone toward groceries, a car payment, or a small emergency fund. Instead, it is flowing directly to the credit card company just because you paid a bill a few days late.The stress does not end with the rate hike. Your credit score takes a hit the moment that late payment is reported to the credit bureaus. A single thirty-day late payment can drop a good credit score by fifty to one hundred points. For a middle-class consumer, that drop can have immediate real-world consequences. If you need to refinance your car loan or apply for a mortgage, a lower score means a higher interest rate. Over the life of a thirty-year mortgage, a one-percentage-point difference in your rate can cost you tens of thousands of dollars. That is a massive hidden tax you pay simply because you forgot to hit the submit button one time.Once your score drops, other dominoes start to fall. Your auto insurance company may raise your premiums because they use credit-based insurance scores to set rates. Your landlord might decide not to renew your lease or require a larger security deposit. You might lose access to the best credit cards with rewards and cash back, forcing you to rely on less favorable products. Each of these consequences adds another layer of financial pressure to your monthly budget.The mental toll is just as heavy. You start dreading the mail. You avoid checking your bank balance. You argue with your spouse about who forgot to pay the bill. The anxiety bleeds into other areas of your life. You find yourself lying awake at night running numbers in your head, trying to figure out how you will cover the next payment. This kind of chronic financial stress is linked to higher rates of depression, insomnia, and even physical health problems like high blood pressure. It strains marriages and makes it harder to focus at work, which can lead to missed opportunities for raises or promotions.For many middle-class families, the late payment is not a sign of irresponsibility. It is a symptom of playing tug of war with too many bills at once. You are juggling a mortgage, a car payment, student loans, childcare costs, and everyday expenses. Something slips through the cracks, and one late payment spirals into a hole that takes months to climb out of. The irony is that the credit card company offers you a way out by letting you pay over time, but the penalty rates and fees make that process much more expensive and stressful than it needs to be.The best way to avoid this entire cascade is to set up automatic payments for at least the minimum amount due on every account. If you are worried about overdraft fees, you can schedule the payment for a day or two after your paycheck hits. You can also set up text or email alerts for upcoming due dates. These simple steps cost nothing and can prevent the domino effect that turns a simple mistake into a long-term financial headache. One late payment is never just one late payment. It is the beginning of a chain that tightens the financial stress around your household until you break it.

A credit limit is the maximum amount you can borrow on a revolving account. Exceeding this limit typically results in fees and can damage your credit score. A lower limit can also force a high credit utilization ratio, which hurts your score.

While enrolling in a DMP may be noted on your credit report, it is not inherently damaging. The accounts included may be closed, which can affect your credit mix and utilization. However, consistent on-time payments through the plan can positively rebuild your score over time.

No. Checking your own credit score is a "soft inquiry," which does not affect your score at all. Only hard inquiries from applications for new credit have an impact.

Yes. Violations of laws like the Truth in Lending Act (TILA) or state usury laws (which cap interest rates) can lead to legal penalties for lenders.

Debt becomes intertwined with major life expenses like a mortgage, costs of raising young children, and potentially higher auto loans. The pressure to save for retirement and children's education increases while disposable income may shrink.