An income shock is exactly what it sounds like: a sudden, unexpected event that significantly reduces the money you have coming in or drastically increases your necessary expenses. It’s a financial jolt that disrupts your normal cash flow, often leaving you scrambling to cover bills you could easily handle just a month before. For middle-class families who typically manage a careful balance between mortgages, car payments, student loans, and saving for the future, an income shock can quickly turn that stability on its head. Understanding what these shocks are and how they work is the first crucial step in building a financial plan that can withstand them.At its core, an income shock hits one of the two main pillars of your household budget: your earnings or your essential costs. On the earnings side, the most direct shock is the loss of a job or a reduction in work hours. But it’s not just unemployment. It could also be a sudden drop in commission for a salesperson, the loss of a crucial client for a freelancer, or an unexpected early retirement. On the expense side, an income shock occurs when an unavoidable cost explodes your budget. A major medical emergency not fully covered by insurance, a critical home repair like a failed roof or furnace, or a large, unexpected car repair bill can all function as an income shock. They force you to redirect money meant for other purposes, creating a gap in your monthly finances.The real danger of an income shock isn’t just the initial event itself, but the domino effect it can trigger, especially when it comes to credit and debt. When your income drops or a giant bill arrives, the first thing many people do is turn to their available credit to bridge the gap. You might put the medical bill on a credit card or skip a credit card payment to cover the mortgage. This is a rational short-term survival tactic, but it can start a costly cycle. High-interest credit card debt begins to accumulate, and minimum payments rise. If the situation lasts, you might miss payments altogether, which damages your credit score. A lower credit score then makes future borrowing more expensive, with higher interest rates on everything from car loans to potential new mortgages, digging the hole even deeper.It’s also important to distinguish an income shock from ordinary, planned expenses. A shock is unanticipated and severe. Budgeting for holiday gifts or saving for a summer vacation is different. You can plan and save for those. An income shock is something you couldn’t—or didn’t—see coming. It’s the difference between your car needing its routine oil change and the transmission failing without warning. The latter is a shock because of its size, timing, and necessity.So, what can you do? The goal is to build buffers between your regular life and these inevitable surprises. This starts with an emergency fund. Financial experts often recommend saving three to six months’ worth of essential living expenses in a separate, easily accessible savings account. This money acts as a shock absorber. When your income drops or a major bill hits, you can use this cash instead of high-interest credit, protecting your financial health and your credit score. For middle-class consumers with many fixed obligations, this fund is not a luxury; it’s a foundational piece of security.Beyond savings, a proactive review of your budget can help. Look for flexible expenses you could cut quickly if needed, like subscription services, dining out, or entertainment. Knowing these levers in advance reduces panic if you need to pull them. Furthermore, understanding the terms of your credit—like the interest rates on your cards or the possibility of requesting a hardship program from a lender—is wise preparation. Finally, consider your insurance coverage. Adequate health, auto, and homeowners or renters insurance are critical defenses against catastrophic expense shocks.In the end, an income shock is a test of financial resilience. While you can’t predict every twist of fate, you can absolutely prepare for the reality that something will eventually happen. By recognizing what an income shock is—a sudden drain on your cash flow—you can take concrete steps today to shield your budget, protect your credit, and ensure that a temporary setback doesn’t turn into a long-term financial crisis. The peace of mind that comes from this preparation is perhaps the most valuable asset of all.

An income shock is exactly what it sounds like: a sudden, unexpected event that significantly reduces the money you have coming in or drastically increases your necessary expenses. It’s a financial jolt that disrupts your normal cash flow, often leaving you scrambling to cover bills you could easily handle just a month before. For middle-class families who typically manage a careful balance between mortgages, car payments, student loans, and saving for the future, an income shock can quickly turn that stability on its head. Understanding what these shocks are and how they work is the first crucial step in building a financial plan that can withstand them.At its core, an income shock hits one of the two main pillars of your household budget: your earnings or your essential costs. On the earnings side, the most direct shock is the loss of a job or a reduction in work hours. But it’s not just unemployment. It could also be a sudden drop in commission for a salesperson, the loss of a crucial client for a freelancer, or an unexpected early retirement. On the expense side, an income shock occurs when an unavoidable cost explodes your budget. A major medical emergency not fully covered by insurance, a critical home repair like a failed roof or furnace, or a large, unexpected car repair bill can all function as an income shock. They force you to redirect money meant for other purposes, creating a gap in your monthly finances.The real danger of an income shock isn’t just the initial event itself, but the domino effect it can trigger, especially when it comes to credit and debt. When your income drops or a giant bill arrives, the first thing many people do is turn to their available credit to bridge the gap. You might put the medical bill on a credit card or skip a credit card payment to cover the mortgage. This is a rational short-term survival tactic, but it can start a costly cycle. High-interest credit card debt begins to accumulate, and minimum payments rise. If the situation lasts, you might miss payments altogether, which damages your credit score. A lower credit score then makes future borrowing more expensive, with higher interest rates on everything from car loans to potential new mortgages, digging the hole even deeper.It’s also important to distinguish an income shock from ordinary, planned expenses. A shock is unanticipated and severe. Budgeting for holiday gifts or saving for a summer vacation is different. You can plan and save for those. An income shock is something you couldn’t—or didn’t—see coming. It’s the difference between your car needing its routine oil change and the transmission failing without warning. The latter is a shock because of its size, timing, and necessity.So, what can you do? The goal is to build buffers between your regular life and these inevitable surprises. This starts with an emergency fund. Financial experts often recommend saving three to six months’ worth of essential living expenses in a separate, easily accessible savings account. This money acts as a shock absorber. When your income drops or a major bill hits, you can use this cash instead of high-interest credit, protecting your financial health and your credit score. For middle-class consumers with many fixed obligations, this fund is not a luxury; it’s a foundational piece of security.Beyond savings, a proactive review of your budget can help. Look for flexible expenses you could cut quickly if needed, like subscription services, dining out, or entertainment. Knowing these levers in advance reduces panic if you need to pull them. Furthermore, understanding the terms of your credit—like the interest rates on your cards or the possibility of requesting a hardship program from a lender—is wise preparation. Finally, consider your insurance coverage. Adequate health, auto, and homeowners or renters insurance are critical defenses against catastrophic expense shocks.In the end, an income shock is a test of financial resilience. While you can’t predict every twist of fate, you can absolutely prepare for the reality that something will eventually happen. By recognizing what an income shock is—a sudden drain on your cash flow—you can take concrete steps today to shield your budget, protect your credit, and ensure that a temporary setback doesn’t turn into a long-term financial crisis. The peace of mind that comes from this preparation is perhaps the most valuable asset of all.

Financial experts recommend starting with a goal of $500 to $1,000 as a initial "starter" fund. This small buffer can cover most common minor emergencies and prevent the need to resort to predatory debt.

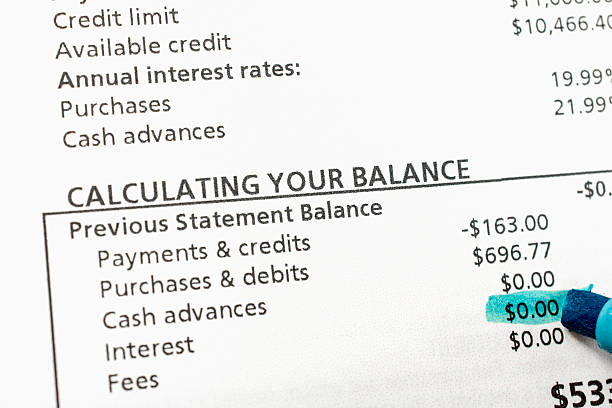

Two popular methods are the "avalanche" method (paying off debts with the highest interest rates first to save the most money) and the "snowball" method (paying off the smallest balances first for psychological wins). For long-term financial health, the avalanche method is typically most effective for those in their 40s.

High deductibles, copays, coinsurance, out-of-network charges, and uncovered services (e.g., dental, vision) can leave patients with significant bills despite having insurance coverage.

Conduct a thorough spending audit. Cancel unused subscriptions, reduce dining out, negotiate lower bills (like insurance or phone plans), and temporarily halt discretionary spending on non-essentials.

Living on a deliberate budget. This is the decade to move from vague spending to intentional allocation of every dollar. A rigorous budget is the essential tool for freeing up cash to attack debt, build savings, and secure your financial future. It's the foundation for recovery and long-term stability.