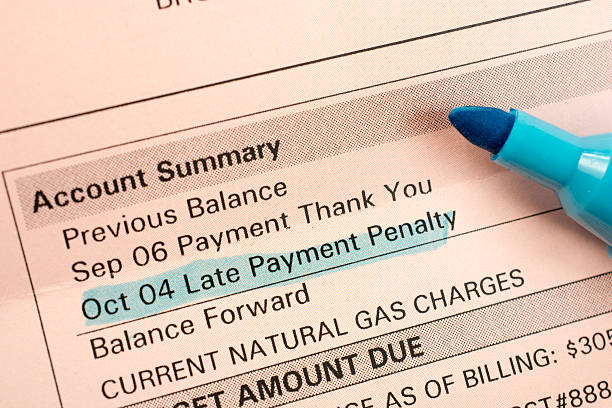

When you start falling behind on credit card payments, the panic is real. You miss one payment, then another. The phone starts ringing with collection calls. Fees pile up. Your minimum payments become impossible to manage. In that moment, many middle-class consumers look for an escape hatch. They find debt settlement companies promising to slash their balances in half. It sounds like a lifeline. But for most people, debt settlement is not the first step you should take. It is often the last resort. Before you ever sign up with a debt settlement firm, you should try credit counseling. It is a prevention strategy that can stop the damage before it gets worse and save you from the long-term consequences that come with settling your debts.Debt settlement works this way. You stop paying your creditors for several months. During that time, you put money into a special account. The debt settlement company then negotiates with your creditors to accept less than the full amount you owe. They might agree to take sixty cents on the dollar or even less. You pay the settlement company a fee, and you walk away with a lower balance. On paper, that sounds like a win. In reality, it comes with serious costs. While you are not paying your credit cards for those months, your credit score takes a massive hit. Late payments get reported to the credit bureaus. Your accounts go to collections. Some creditors may sue you to collect the full amount. And the debt you settle, the amount that gets written off, is often treated as taxable income by the IRS. You could get a surprise tax bill the following year for money you never actually received.Credit counseling avoids most of this trouble. When you go to a nonprofit credit counseling agency, you sit down with a trained counselor who reviews your entire financial picture. They look at your income, your expenses, and your debts. They help you create a realistic budget. For many people, that alone is enough to get back on track. The counselor can show you where your money is going and help you find hidden waste you never noticed before. But credit counseling goes further. If your debts are too high to manage even with a better budget, the agency can enroll you in a debt management plan. Under this plan, you make one monthly payment to the agency. They distribute that money to your creditors. More importantly, they negotiate with your creditors on your behalf to lower your interest rates and waive late fees. You still pay back the full amount you owe, but the process becomes manageable because the interest stops piling up so fast.The difference between credit counseling and debt settlement is fundamental. Credit counseling is designed to prevent the worst outcomes. It keeps your credit score from completely collapsing. It avoids lawsuits. It stops collection calls. It gives you a structured path to becoming debt free without the harsh penalties that come with settlement. Debt settlement, by contrast, assumes you have already hit rock bottom. It is a strategy for people who have no other choice and are willing to accept the damage to their credit and financial reputation.For a middle-class consumer with steady income and a desire to fix the problem, credit counseling should always come first. It is a prevention strategy because it stops the situation from deteriorating further. It prevents you from harming your credit score for years. It prevents you from being sued by creditors. It prevents the tax consequences that come with forgiven debt. And it prevents you from spending money on fees that often produce no results. Many debt settlement companies charge high upfront fees, and there is no guarantee they will actually settle all your debts. Some people pay thousands of dollars in fees only to find themselves in worse shape than when they started.You can find a reputable credit counseling agency easily. Look for one that is nonprofit and accredited by the National Foundation for Credit Counseling or the Financial Counseling Association of America. The first session is usually free or low cost. The counselor is not there to sell you anything. They are there to help you understand your options. If a debt management plan makes sense, they will explain the costs and the timeline. If it does not make sense, they will tell you that as well.Debt settlement is a real option, but it is a dangerous one. Think of it as a fire extinguisher you break out only when the house is already burning down. For most people, the smoke alarm of missed payments and late fees can be handled with a much less destructive tool. That tool is credit counseling. Before you give up on your credit history and your financial future, take that first step. It could prevent you from making a decision you will regret for years.

When you start falling behind on credit card payments, the panic is real. You miss one payment, then another. The phone starts ringing with collection calls. Fees pile up. Your minimum payments become impossible to manage. In that moment, many middle-class consumers look for an escape hatch. They find debt settlement companies promising to slash their balances in half. It sounds like a lifeline. But for most people, debt settlement is not the first step you should take. It is often the last resort. Before you ever sign up with a debt settlement firm, you should try credit counseling. It is a prevention strategy that can stop the damage before it gets worse and save you from the long-term consequences that come with settling your debts.Debt settlement works this way. You stop paying your creditors for several months. During that time, you put money into a special account. The debt settlement company then negotiates with your creditors to accept less than the full amount you owe. They might agree to take sixty cents on the dollar or even less. You pay the settlement company a fee, and you walk away with a lower balance. On paper, that sounds like a win. In reality, it comes with serious costs. While you are not paying your credit cards for those months, your credit score takes a massive hit. Late payments get reported to the credit bureaus. Your accounts go to collections. Some creditors may sue you to collect the full amount. And the debt you settle, the amount that gets written off, is often treated as taxable income by the IRS. You could get a surprise tax bill the following year for money you never actually received.Credit counseling avoids most of this trouble. When you go to a nonprofit credit counseling agency, you sit down with a trained counselor who reviews your entire financial picture. They look at your income, your expenses, and your debts. They help you create a realistic budget. For many people, that alone is enough to get back on track. The counselor can show you where your money is going and help you find hidden waste you never noticed before. But credit counseling goes further. If your debts are too high to manage even with a better budget, the agency can enroll you in a debt management plan. Under this plan, you make one monthly payment to the agency. They distribute that money to your creditors. More importantly, they negotiate with your creditors on your behalf to lower your interest rates and waive late fees. You still pay back the full amount you owe, but the process becomes manageable because the interest stops piling up so fast.The difference between credit counseling and debt settlement is fundamental. Credit counseling is designed to prevent the worst outcomes. It keeps your credit score from completely collapsing. It avoids lawsuits. It stops collection calls. It gives you a structured path to becoming debt free without the harsh penalties that come with settlement. Debt settlement, by contrast, assumes you have already hit rock bottom. It is a strategy for people who have no other choice and are willing to accept the damage to their credit and financial reputation.For a middle-class consumer with steady income and a desire to fix the problem, credit counseling should always come first. It is a prevention strategy because it stops the situation from deteriorating further. It prevents you from harming your credit score for years. It prevents you from being sued by creditors. It prevents the tax consequences that come with forgiven debt. And it prevents you from spending money on fees that often produce no results. Many debt settlement companies charge high upfront fees, and there is no guarantee they will actually settle all your debts. Some people pay thousands of dollars in fees only to find themselves in worse shape than when they started.You can find a reputable credit counseling agency easily. Look for one that is nonprofit and accredited by the National Foundation for Credit Counseling or the Financial Counseling Association of America. The first session is usually free or low cost. The counselor is not there to sell you anything. They are there to help you understand your options. If a debt management plan makes sense, they will explain the costs and the timeline. If it does not make sense, they will tell you that as well.Debt settlement is a real option, but it is a dangerous one. Think of it as a fire extinguisher you break out only when the house is already burning down. For most people, the smoke alarm of missed payments and late fees can be handled with a much less destructive tool. That tool is credit counseling. Before you give up on your credit history and your financial future, take that first step. It could prevent you from making a decision you will regret for years.

Be honest and concise. Explain your situation clearly, specify that you are seeking hardship assistance, and have details about your income, expenses, and hardship documentation ready.

Create a detailed post-divorce budget based on your individual income and expenses. This clarifies your new financial reality and helps identify potential overextension risks early.

Non-profit credit counseling agencies can provide invaluable guidance. They can review your situation, help you understand if you're a candidate for a consolidation loan or balance transfer, and may even offer a Debt Management Plan (DMP) with better terms through relationships with creditors.

It locks you into a higher cost of living. You become dependent on your current income level to maintain your lifestyle, making it difficult to take career risks, start a business, or weather a job loss without severe financial strain.

Your DTI ratio is your total monthly debt payments divided by your gross monthly income, expressed as a percentage. It is a key metric lenders use to assess your risk. A DTI above 36% is often seen as a warning sign of overextension, and above 43% typically makes qualifying for new credit very difficult.