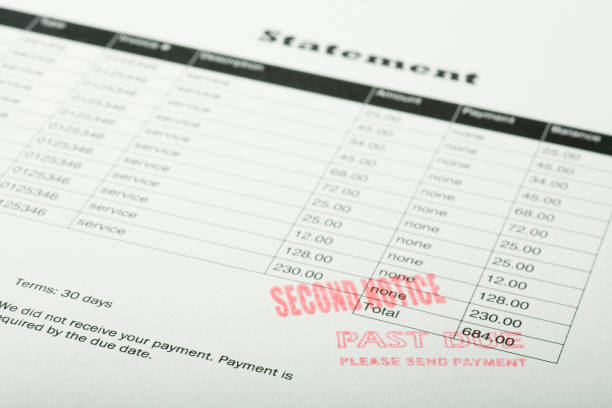

The intersection of health and finance creates a uniquely stressful burden for millions of Americans. Medical debt, often incurred unexpectedly and through no fault of the individual, carries significant weight in the financial ecosystem, with one of its most profound impacts being on personal credit scores. Understanding this relationship is crucial, as a credit score is more than just a number; it is a gatekeeper for housing, transportation, and future financial opportunities. The impact of medical debt on this critical metric is complex, shaped by both standard credit reporting practices and recent industry reforms designed to mitigate its harshest effects.Fundamentally, medical debt impacts credit scores in the same way as other types of consumer debt: through delinquency and collection accounts. When a medical bill is not paid, the healthcare provider may eventually sell that debt to a third-party collection agency. This collection agency then reports the delinquent account to the three major credit bureaus—Equifax, Experian, and TransUnion. Once listed, a collection account can severely damage a credit score, as payment history is the single most influential factor in score calculations, comprising 35% of a FICO score. A single collection account can cause a drop of 50 to 100 points, pushing consumers from good or excellent credit into fair or poor territory. This downgrade can trigger higher interest rates on loans, denial of rental applications, or even affect employment prospects.However, the reporting of medical debt has several distinctive characteristics that differentiate it from credit card or loan debt. Recognizing that medical expenses are often unforeseen and involuntary, the national credit bureaus implemented key changes in recent years. Most significantly, as of 2022, paid medical collection debt is no longer included on consumer credit reports. Furthermore, the time before unpaid medical debt appears on reports was extended from six months to one year, providing a longer grace period for individuals to resolve bills with insurance companies or set up payment plans. Perhaps most impactful is the 2023 announcement that medical collection debt under $500 would no longer be reported. These reforms acknowledge the unique nature of medical bills and have spared many consumers from the lasting scar of small, often confusing, medical debts.Despite these improvements, significant challenges remain. Large unpaid medical bills that go to collections will still be reported after the one-year waiting period. The mere presence of a collection account, regardless of the amount, signals risk to lenders and can suppress credit scores. Furthermore, the path from hospital to collection agency is fraught with complexity. Bills may be sent to collections due to insurance processing delays or errors, not because a patient is refusing to pay. Consumers often find themselves navigating a labyrinth of provider bills and insurance explanations of benefits, and a simple administrative mistake can inadvertently lead to a collections mark. This opacity makes medical debt particularly pernicious.The consequences of a lowered credit score due to medical debt create a vicious cycle. The resulting higher interest rates on auto loans or credit cards can strain a budget already stretched thin by healthcare costs. It may become more difficult to secure affordable housing or finance a reliable car needed to get to work or medical appointments. This financial stress can, ironically, exacerbate health issues, creating a feedback loop where poor health leads to debt, which harms credit, which in turn creates more stress and worse financial health.In conclusion, medical debt impacts credit scores through the traditional mechanism of collection accounts, but its influence is tempered by evolving industry standards that recognize its involuntary nature. While reforms have lessened the burden of smaller and paid medical collections, substantial unpaid debts continue to pose a major threat to creditworthiness. The enduring impact highlights a systemic issue where a health crisis can rapidly morph into a long-term financial crisis, undermining economic stability and mobility. For consumers, vigilance in reviewing medical bills, communicating with providers, and monitoring credit reports is essential to mitigate the damaging chain reaction that begins with an unexpected medical bill.

The intersection of health and finance creates a uniquely stressful burden for millions of Americans. Medical debt, often incurred unexpectedly and through no fault of the individual, carries significant weight in the financial ecosystem, with one of its most profound impacts being on personal credit scores. Understanding this relationship is crucial, as a credit score is more than just a number; it is a gatekeeper for housing, transportation, and future financial opportunities. The impact of medical debt on this critical metric is complex, shaped by both standard credit reporting practices and recent industry reforms designed to mitigate its harshest effects.Fundamentally, medical debt impacts credit scores in the same way as other types of consumer debt: through delinquency and collection accounts. When a medical bill is not paid, the healthcare provider may eventually sell that debt to a third-party collection agency. This collection agency then reports the delinquent account to the three major credit bureaus—Equifax, Experian, and TransUnion. Once listed, a collection account can severely damage a credit score, as payment history is the single most influential factor in score calculations, comprising 35% of a FICO score. A single collection account can cause a drop of 50 to 100 points, pushing consumers from good or excellent credit into fair or poor territory. This downgrade can trigger higher interest rates on loans, denial of rental applications, or even affect employment prospects.However, the reporting of medical debt has several distinctive characteristics that differentiate it from credit card or loan debt. Recognizing that medical expenses are often unforeseen and involuntary, the national credit bureaus implemented key changes in recent years. Most significantly, as of 2022, paid medical collection debt is no longer included on consumer credit reports. Furthermore, the time before unpaid medical debt appears on reports was extended from six months to one year, providing a longer grace period for individuals to resolve bills with insurance companies or set up payment plans. Perhaps most impactful is the 2023 announcement that medical collection debt under $500 would no longer be reported. These reforms acknowledge the unique nature of medical bills and have spared many consumers from the lasting scar of small, often confusing, medical debts.Despite these improvements, significant challenges remain. Large unpaid medical bills that go to collections will still be reported after the one-year waiting period. The mere presence of a collection account, regardless of the amount, signals risk to lenders and can suppress credit scores. Furthermore, the path from hospital to collection agency is fraught with complexity. Bills may be sent to collections due to insurance processing delays or errors, not because a patient is refusing to pay. Consumers often find themselves navigating a labyrinth of provider bills and insurance explanations of benefits, and a simple administrative mistake can inadvertently lead to a collections mark. This opacity makes medical debt particularly pernicious.The consequences of a lowered credit score due to medical debt create a vicious cycle. The resulting higher interest rates on auto loans or credit cards can strain a budget already stretched thin by healthcare costs. It may become more difficult to secure affordable housing or finance a reliable car needed to get to work or medical appointments. This financial stress can, ironically, exacerbate health issues, creating a feedback loop where poor health leads to debt, which harms credit, which in turn creates more stress and worse financial health.In conclusion, medical debt impacts credit scores through the traditional mechanism of collection accounts, but its influence is tempered by evolving industry standards that recognize its involuntary nature. While reforms have lessened the burden of smaller and paid medical collections, substantial unpaid debts continue to pose a major threat to creditworthiness. The enduring impact highlights a systemic issue where a health crisis can rapidly morph into a long-term financial crisis, undermining economic stability and mobility. For consumers, vigilance in reviewing medical bills, communicating with providers, and monitoring credit reports is essential to mitigate the damaging chain reaction that begins with an unexpected medical bill.

The goal is to reduce your PTI to a level where your debt payments are comfortable and not a source of constant financial stress. Achieving a PTI below 10% provides tremendous flexibility, allowing you to confidently save for emergencies, invest for the future, and withstand financial shocks.

Leaving joint accounts open risks new charges by an ex-spouse, increasing your liability. Converting joint accounts to individual ones protects your credit and prevents further shared debt accumulation.

Options include: 1) Selling the asset (if you have positive equity), 2) Voluntary surrender (returning the asset to the lender, though you may still owe a deficiency balance), 3) Refinancing (if you qualify for a lower payment), or 4) Negotiating a short sale (for a home, where the lender agrees to a sale for less than the owed amount).

Depending on state laws, a creditor with a judgment may be able to place a lien on your property (like your home) or levy (seize) funds from your bank accounts.

Yes. In some cultures, displaying wealth through gifts, weddings, or possessions is deeply tied to social respect and family honor, increasing the pressure to spend even when it leads to debt.