In an era defined by readily available credit and complex financial products, the specter of debt overextension looms large for many. While numerous strategies exist to manage existing liabilities, the most effective first step to prevent the problem altogether is not found in a loan document or a consolidation plan, but in a foundational act of self-awareness: the creation and meticulous maintenance of a detailed personal budget. This proactive measure serves as the essential map and compass for one’s financial journey, transforming abstract income and expenses into a clear, actionable plan that inherently guards against spending beyond one’s means.The primary power of budgeting as a preventative tool lies in its capacity to illuminate reality. Without a budget, financial decisions are often made in a vacuum, guided by the fluctuating balance of a checking account rather than true fiscal capacity. This leads to the dangerous illusion that available cash equates to available spending power, a misconception that ignores fixed obligations and future needs. A comprehensive budget shatters this illusion by forcing an individual to account for every dollar earned and to assign each a specific purpose before it is spent—a process known as zero-based budgeting. This practice creates a crucial pause between impulse and action, establishing a framework where discretionary spending is consciously limited to what remains after necessities and savings are secured. By defining these boundaries upfront, the budget acts as a pre-emptive barrier, making it far more difficult to inadvertently drift into overextension.Furthermore, an effective budget transcends mere tracking to become a tool for strategic prioritization, which is the heart of debt prevention. It requires an individual to distinguish between essential needs and non-essential wants, a fundamental skill for sustainable financial health. When one sees clearly that monthly debt service payments—whether for a mortgage, car loan, or student debt—consume a specific, significant portion of their income, it naturally encourages more prudent decisions before taking on additional liabilities. The budget answers the critical question, “Can I afford this?“ with hard data rather than optimistic guesswork. It reveals whether a new car payment would strain the grocery allotment or if financing a vacation would jeopardize the ability to pay utilities. This visibility allows for informed, intentional choices that align with long-term stability rather than short-term gratification, thereby avoiding the incremental commitments that collectively lead to overextension.Critically, a well-constructed budget also integrates the building of financial resilience, addressing the very emergencies that often force people into high-interest debt. By categorizing savings—for an emergency fund, routine maintenance, and future goals—as non-negotiable “expenses,“ the budget ensures these buffers are consistently funded. This transforms the budget from a restrictive document into an empowering one. When an unexpected medical bill or car repair arises, the solution comes from a dedicated savings category, not a credit card that could begin a cycle of costly revolving debt. This proactive saving fundamentally alters one’s financial trajectory, breaking the reactive cycle of using debt to cover life’s inevitable surprises.Ultimately, the act of budgeting establishes a mindset of intentionality and control. It is a declarative first step that moves an individual from being a passive observer of their finances to an active manager. This habitual engagement fosters greater financial literacy, as one becomes intimately familiar with their cash flow patterns, spending triggers, and saving capabilities. While tools like debt counseling or consolidation plans are valuable for addressing existing problems, they are reactive. The personal budget is uniquely proactive. It does not merely treat the symptoms of debt overextension; it systematically inoculates against the condition by creating a living financial plan that respects income limits, prioritizes obligations, and plans for the unforeseen. Therefore, before seeking credit, making a major purchase, or even setting financial goals, the most effective and essential first step toward a debt-free future is to diligently craft and commit to a realistic, detailed personal budget.

In an era defined by readily available credit and complex financial products, the specter of debt overextension looms large for many. While numerous strategies exist to manage existing liabilities, the most effective first step to prevent the problem altogether is not found in a loan document or a consolidation plan, but in a foundational act of self-awareness: the creation and meticulous maintenance of a detailed personal budget. This proactive measure serves as the essential map and compass for one’s financial journey, transforming abstract income and expenses into a clear, actionable plan that inherently guards against spending beyond one’s means.The primary power of budgeting as a preventative tool lies in its capacity to illuminate reality. Without a budget, financial decisions are often made in a vacuum, guided by the fluctuating balance of a checking account rather than true fiscal capacity. This leads to the dangerous illusion that available cash equates to available spending power, a misconception that ignores fixed obligations and future needs. A comprehensive budget shatters this illusion by forcing an individual to account for every dollar earned and to assign each a specific purpose before it is spent—a process known as zero-based budgeting. This practice creates a crucial pause between impulse and action, establishing a framework where discretionary spending is consciously limited to what remains after necessities and savings are secured. By defining these boundaries upfront, the budget acts as a pre-emptive barrier, making it far more difficult to inadvertently drift into overextension.Furthermore, an effective budget transcends mere tracking to become a tool for strategic prioritization, which is the heart of debt prevention. It requires an individual to distinguish between essential needs and non-essential wants, a fundamental skill for sustainable financial health. When one sees clearly that monthly debt service payments—whether for a mortgage, car loan, or student debt—consume a specific, significant portion of their income, it naturally encourages more prudent decisions before taking on additional liabilities. The budget answers the critical question, “Can I afford this?“ with hard data rather than optimistic guesswork. It reveals whether a new car payment would strain the grocery allotment or if financing a vacation would jeopardize the ability to pay utilities. This visibility allows for informed, intentional choices that align with long-term stability rather than short-term gratification, thereby avoiding the incremental commitments that collectively lead to overextension.Critically, a well-constructed budget also integrates the building of financial resilience, addressing the very emergencies that often force people into high-interest debt. By categorizing savings—for an emergency fund, routine maintenance, and future goals—as non-negotiable “expenses,“ the budget ensures these buffers are consistently funded. This transforms the budget from a restrictive document into an empowering one. When an unexpected medical bill or car repair arises, the solution comes from a dedicated savings category, not a credit card that could begin a cycle of costly revolving debt. This proactive saving fundamentally alters one’s financial trajectory, breaking the reactive cycle of using debt to cover life’s inevitable surprises.Ultimately, the act of budgeting establishes a mindset of intentionality and control. It is a declarative first step that moves an individual from being a passive observer of their finances to an active manager. This habitual engagement fosters greater financial literacy, as one becomes intimately familiar with their cash flow patterns, spending triggers, and saving capabilities. While tools like debt counseling or consolidation plans are valuable for addressing existing problems, they are reactive. The personal budget is uniquely proactive. It does not merely treat the symptoms of debt overextension; it systematically inoculates against the condition by creating a living financial plan that respects income limits, prioritizes obligations, and plans for the unforeseen. Therefore, before seeking credit, making a major purchase, or even setting financial goals, the most effective and essential first step toward a debt-free future is to diligently craft and commit to a realistic, detailed personal budget.

If you are consistently missing other payments to keep up with the car loan, have been denied refinancing, or are considering repossession, contact a non-profit credit counseling agency for guidance.

Yes, but providers typically require multiple notices and must follow state regulations. Shut-offs are often a last resort, especially for essential services like electricity or water.

It's sensible for planned, essential purchases that you can already afford but would prefer to smooth out over a few paychecks. Examples include replacing a broken appliance, buying necessary work attire, or purchasing a specific item that is on a deep sale.

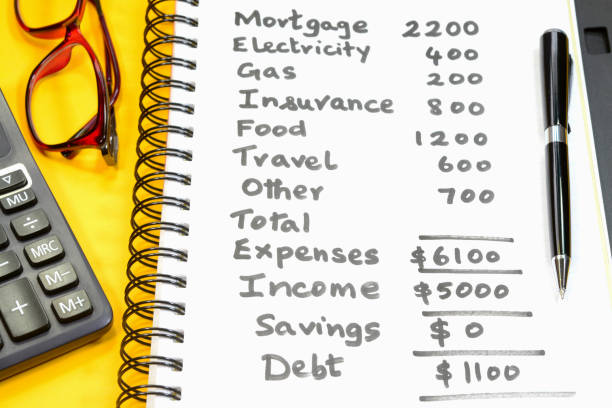

Your DTI ratio is your total monthly debt payments divided by your gross monthly income, expressed as a percentage. It is a key metric lenders use to assess your risk. A DTI above 36% is often seen as a warning sign of overextension, and above 43% typically makes qualifying for new credit very difficult.

Some cards charge an annual fee. For debt management, a fee may be worth paying if the savings on interest (e.g., from a long 0% APR period) significantly exceed the fee cost. Always do the math.