We all want to feel successful and respected. For many of us, that feeling gets tied to what we own—the car in the driveway, the watch on our wrist, the label on our clothes. This is not just vanity. It is a deeply human instinct to signal our place in the world. But when that instinct crosses into conspicuous consumption—spending money on expensive items mainly to show them off—it can quietly wreck your finances. The cost is not just the price tag. It is the compounding effect on your savings, your debt, and your long-term goals.Conspicuous consumption is a term that goes back more than a century, but it has never been more powerful than today. Social media has turned our lives into public galleries. Every vacation, every new purchase, every meal out can become a post. And while you might think you are just sharing your life, you are also sending a signal. Worse, you are receiving signals from everyone else. This constant comparison creates a pressure to spend money you do not have on things you do not need, just to keep up.The trap works like this. You see a coworker driving a new SUV. You start thinking your five-year-old sedan looks old. Even if it runs perfectly, you feel a nagging sense of falling behind. Maybe you get a bonus or a raise. Instead of using that extra money to pay down credit card debt or build your emergency fund, you buy a newer car. The monthly payment eats into your cash flow. But you tell yourself you deserve it. That is the first step down a dangerous path.What makes conspicuous consumption especially tricky is that it often feels rational in the moment. You might tell yourself the new phone will make you more productive, or the designer bag is an investment piece that will last forever. But the real motivation is usually social: you want others to see you as successful. Studies in behavioral economics show that people often spend more on visible goods than on things that actually improve their quality of life. They will buy a luxury watch but skip dental checkups. They will lease a high-end car but have no retirement savings. The visible items give a quick hit of status, but the invisible costs—interest payments, missed investment growth, financial stress—grow silently.Another hidden cost is what economists call the “hedonic treadmill.“ When you buy a flashy new item, the happiness boost fades quickly. You get used to the new car, the new kitchen, the new handbag. Then you need an even bigger purchase to get the same thrill. This is why people who fall into the trap of conspicuous consumption often feel like they can never get ahead. No matter how much they spend, there is always someone with more. The money goes out, but the satisfaction does not last.For middle-class consumers, the danger is especially high because you have enough income to qualify for loans but not enough wealth to absorb mistakes. You can easily finance a lifestyle you cannot really afford. Credit cards and auto loans make it easy to buy now and pay later. But later comes with interest. If you are spending 15 or 20 percent of your income on car payments and credit card minimums just to keep up appearances, you are robbing your future self. You lose the ability to save for a down payment on a house, to invest in your retirement, or to handle an emergency without going deeper into debt.The solution is not to become a miser or to stop caring about quality. But it does mean being honest about why you are buying something. Before any significant purchase, ask yourself: Would I buy this if nobody else would ever see it? If the answer is no, then you are buying for status, not for function. That does not mean you should never treat yourself. But when status becomes the main driver, you should pause. Consider the trade-off. That $50,000 luxury SUV could be a $30,000 reliable car plus $20,000 in a savings account earning compound interest. Over ten years, that difference could be life-changing.It also helps to redefine what status means to you. True financial confidence does not come from a logo. It comes from knowing you have options. Having an emergency fund, low debt, and growing investments gives you a quiet kind of status that nobody sees but everyone respects. Instead of trying to impress strangers, focus on building a life that gives you real security.Conspicuous consumption is a powerful force, but it is one you can control. Once you recognize the hidden costs—the debt, the stress, the lost opportunities—it becomes easier to say no to the impulse. Spend money on what truly matters, not on what looks good. Your bank account and your peace of mind will thank you.

We all want to feel successful and respected. For many of us, that feeling gets tied to what we own—the car in the driveway, the watch on our wrist, the label on our clothes. This is not just vanity. It is a deeply human instinct to signal our place in the world. But when that instinct crosses into conspicuous consumption—spending money on expensive items mainly to show them off—it can quietly wreck your finances. The cost is not just the price tag. It is the compounding effect on your savings, your debt, and your long-term goals.Conspicuous consumption is a term that goes back more than a century, but it has never been more powerful than today. Social media has turned our lives into public galleries. Every vacation, every new purchase, every meal out can become a post. And while you might think you are just sharing your life, you are also sending a signal. Worse, you are receiving signals from everyone else. This constant comparison creates a pressure to spend money you do not have on things you do not need, just to keep up.The trap works like this. You see a coworker driving a new SUV. You start thinking your five-year-old sedan looks old. Even if it runs perfectly, you feel a nagging sense of falling behind. Maybe you get a bonus or a raise. Instead of using that extra money to pay down credit card debt or build your emergency fund, you buy a newer car. The monthly payment eats into your cash flow. But you tell yourself you deserve it. That is the first step down a dangerous path.What makes conspicuous consumption especially tricky is that it often feels rational in the moment. You might tell yourself the new phone will make you more productive, or the designer bag is an investment piece that will last forever. But the real motivation is usually social: you want others to see you as successful. Studies in behavioral economics show that people often spend more on visible goods than on things that actually improve their quality of life. They will buy a luxury watch but skip dental checkups. They will lease a high-end car but have no retirement savings. The visible items give a quick hit of status, but the invisible costs—interest payments, missed investment growth, financial stress—grow silently.Another hidden cost is what economists call the “hedonic treadmill.“ When you buy a flashy new item, the happiness boost fades quickly. You get used to the new car, the new kitchen, the new handbag. Then you need an even bigger purchase to get the same thrill. This is why people who fall into the trap of conspicuous consumption often feel like they can never get ahead. No matter how much they spend, there is always someone with more. The money goes out, but the satisfaction does not last.For middle-class consumers, the danger is especially high because you have enough income to qualify for loans but not enough wealth to absorb mistakes. You can easily finance a lifestyle you cannot really afford. Credit cards and auto loans make it easy to buy now and pay later. But later comes with interest. If you are spending 15 or 20 percent of your income on car payments and credit card minimums just to keep up appearances, you are robbing your future self. You lose the ability to save for a down payment on a house, to invest in your retirement, or to handle an emergency without going deeper into debt.The solution is not to become a miser or to stop caring about quality. But it does mean being honest about why you are buying something. Before any significant purchase, ask yourself: Would I buy this if nobody else would ever see it? If the answer is no, then you are buying for status, not for function. That does not mean you should never treat yourself. But when status becomes the main driver, you should pause. Consider the trade-off. That $50,000 luxury SUV could be a $30,000 reliable car plus $20,000 in a savings account earning compound interest. Over ten years, that difference could be life-changing.It also helps to redefine what status means to you. True financial confidence does not come from a logo. It comes from knowing you have options. Having an emergency fund, low debt, and growing investments gives you a quiet kind of status that nobody sees but everyone respects. Instead of trying to impress strangers, focus on building a life that gives you real security.Conspicuous consumption is a powerful force, but it is one you can control. Once you recognize the hidden costs—the debt, the stress, the lost opportunities—it becomes easier to say no to the impulse. Spend money on what truly matters, not on what looks good. Your bank account and your peace of mind will thank you.

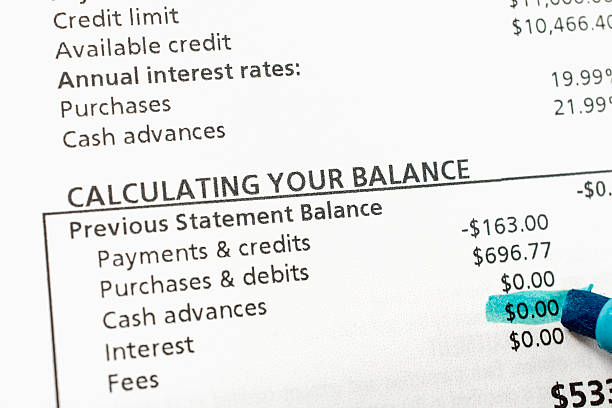

Key fees include late payment fees, over-the-limit fees, and foreign transaction fees. Understanding these penalties is essential to avoid unexpected costs that add to your debt burden.

Federal law limits garnishment to the lesser of 25% of your disposable earnings (after taxes) or the amount by which your weekly income exceeds 30 times the federal minimum wage. Some debts, like child support or taxes, may allow higher limits.

Leasing often means perpetual car payments. The most debt-savvy move is to buy a reliable used car with cash or a short-term loan after your lease ends, freeing up that monthly payment for other goals.

Avoid turning to high-cost solutions like payday loans or title loans, as they create a much worse debt trap. Also, avoid closing old credit cards, as this hurts your credit utilization ratio. Most importantly, avoid ignoring the problem.

It requires treating childcare as a fixed, non-negotiable expense in the budget. This often means drastically reducing other discretionary spending, seeking less expensive care options, or adjusting work schedules to reduce hours needed.