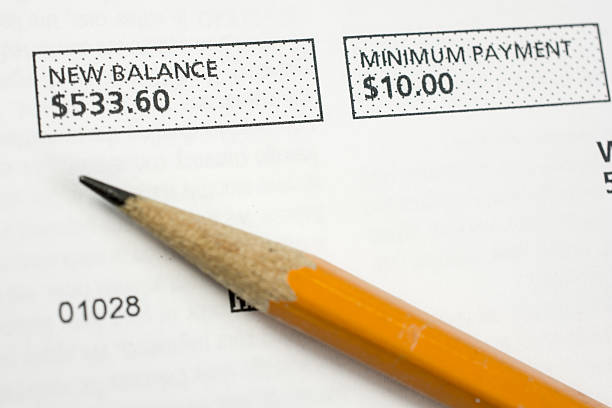

Many diligent credit users believe that paying off their credit card balance immediately after every purchase is the safest, most responsible way to build excellent credit. It makes intuitive sense. If you never carry a balance, you never pay interest, and you avoid the risk of overspending. However, when it comes to your credit score, this habit can actually work against you in a subtle way. The concept that causes this confusing situation is credit utilization, and understanding how it interacts with your statement cycle is one of the most powerful secrets to maximizing your score.Credit utilization is simply the ratio of how much credit you are using compared to how much credit you have available. If you have a total credit limit of ten thousand dollars across all your cards and you currently owe two thousand dollars, your utilization is twenty percent. Most people know that keeping this number below thirty percent is a good rule of thumb. But fewer people understand that the number reported to the credit bureaus is not the number on the screen when you log into your account. It is almost always the balance that appears on your monthly statement.Here is where the confusion begins. When you pay your card off completely before the statement even generates, your statement balance will show as zero. You have no utilization to report. While a zero balance sounds like the perfect financial picture, credit scoring models actually prefer to see a small, active balance. They want evidence that you use credit responsibly, not that you avoid it entirely. FICO and VantageScore models tend to treat a zero utilization rate slightly differently than they treat a very low utilization rate. A tiny utilization, such as one to three percent, often scores a few points higher than a flat zero.This does not mean you should pay interest by carrying a balance month to month. Carrying a balance is never necessary and is always a waste of money. The trick is to let a small balance post to your statement, then pay that statement balance in full before the due date. You get the best of both worlds. You show the credit bureaus that you are using your available credit, which proves you can manage debt, but you never pay a dime of interest because you pay the entire statement amount before the grace period ends.A common myth is that you need to use a large percentage of your limit to show activity, but this is incorrect. Even a very small purchase posting to your statement will accomplish the goal. Let us say you have a credit card with a five thousand dollar limit. If you buy a cup of coffee for two dollars and let that charge appear on your statement before you pay it off, your utilization is essentially zero point zero four percent. That is perfectly fine. It is not necessary to hit the recommended one to ten percent range of your limit. Any non-zero amount is generally beneficial compared to a complete zero.Another mistake people make is paying their card down to zero right before a major credit application, such as a mortgage or auto loan. This seems logical because you want the lowest debt possible. However, if you pay everything to zero, you may cause a temporary drop in your score due to that zero utilization phenomenon. The better strategy is to pay your balances down to a very small amount, roughly one percent of your total credit limit, and let that report for the month or two before you apply for new credit. This gives the scoring model exactly what it wants to see.It is also worth noting that utilization has no memory. Your score reflects your most recently reported utilization from each account. This means you can manipulate your utilization deliberately in the months leading up to an important loan application without any lasting penalty. If you normally carry a high balance for convenience, you can pay it down early for one or two statements and then return to your normal habits. The score impact is immediate and reversible.Ultimately, the goal is not to avoid credit cards, nor is it to use them recklessly. The goal is to use them in a way that creates the most favorable snapshot for the credit bureaus. Letting a small balance appear on your statement before paying it off is a simple, cost-free adjustment to your payment timing. It requires no change in your spending habits, no increase in debt, and no extra fees. It simply requires you to shift your payment date to after the statement closes rather than before. This single change can lift your score by a handful of points, and over the lifespan of a thirty year mortgage, those points can save you thousands of dollars in interest.

Many diligent credit users believe that paying off their credit card balance immediately after every purchase is the safest, most responsible way to build excellent credit. It makes intuitive sense. If you never carry a balance, you never pay interest, and you avoid the risk of overspending. However, when it comes to your credit score, this habit can actually work against you in a subtle way. The concept that causes this confusing situation is credit utilization, and understanding how it interacts with your statement cycle is one of the most powerful secrets to maximizing your score.Credit utilization is simply the ratio of how much credit you are using compared to how much credit you have available. If you have a total credit limit of ten thousand dollars across all your cards and you currently owe two thousand dollars, your utilization is twenty percent. Most people know that keeping this number below thirty percent is a good rule of thumb. But fewer people understand that the number reported to the credit bureaus is not the number on the screen when you log into your account. It is almost always the balance that appears on your monthly statement.Here is where the confusion begins. When you pay your card off completely before the statement even generates, your statement balance will show as zero. You have no utilization to report. While a zero balance sounds like the perfect financial picture, credit scoring models actually prefer to see a small, active balance. They want evidence that you use credit responsibly, not that you avoid it entirely. FICO and VantageScore models tend to treat a zero utilization rate slightly differently than they treat a very low utilization rate. A tiny utilization, such as one to three percent, often scores a few points higher than a flat zero.This does not mean you should pay interest by carrying a balance month to month. Carrying a balance is never necessary and is always a waste of money. The trick is to let a small balance post to your statement, then pay that statement balance in full before the due date. You get the best of both worlds. You show the credit bureaus that you are using your available credit, which proves you can manage debt, but you never pay a dime of interest because you pay the entire statement amount before the grace period ends.A common myth is that you need to use a large percentage of your limit to show activity, but this is incorrect. Even a very small purchase posting to your statement will accomplish the goal. Let us say you have a credit card with a five thousand dollar limit. If you buy a cup of coffee for two dollars and let that charge appear on your statement before you pay it off, your utilization is essentially zero point zero four percent. That is perfectly fine. It is not necessary to hit the recommended one to ten percent range of your limit. Any non-zero amount is generally beneficial compared to a complete zero.Another mistake people make is paying their card down to zero right before a major credit application, such as a mortgage or auto loan. This seems logical because you want the lowest debt possible. However, if you pay everything to zero, you may cause a temporary drop in your score due to that zero utilization phenomenon. The better strategy is to pay your balances down to a very small amount, roughly one percent of your total credit limit, and let that report for the month or two before you apply for new credit. This gives the scoring model exactly what it wants to see.It is also worth noting that utilization has no memory. Your score reflects your most recently reported utilization from each account. This means you can manipulate your utilization deliberately in the months leading up to an important loan application without any lasting penalty. If you normally carry a high balance for convenience, you can pay it down early for one or two statements and then return to your normal habits. The score impact is immediate and reversible.Ultimately, the goal is not to avoid credit cards, nor is it to use them recklessly. The goal is to use them in a way that creates the most favorable snapshot for the credit bureaus. Letting a small balance appear on your statement before paying it off is a simple, cost-free adjustment to your payment timing. It requires no change in your spending habits, no increase in debt, and no extra fees. It simply requires you to shift your payment date to after the statement closes rather than before. This single change can lift your score by a handful of points, and over the lifespan of a thirty year mortgage, those points can save you thousands of dollars in interest.

Prioritize utilities to avoid service disconnection, which can compound crises (e.g., losing heating in winter). Then address high-interest debts like credit cards.

Yes, budgeting apps like Mint or YNAB, and educational platforms like Khan Academy, offer free tools to track spending, create budgets, and learn basic finance concepts.

Nonprofit credit counselors, patient advocacy groups, and legal aid organizations can help negotiate bills, navigate financial assistance, and address collections issues.

It's a balancing act, not an all-or-nothing race. Build a small emergency fund ($1,000) first to avoid going deeper into debt from an unexpected expense. Then, split your extra money between debt repayment and other savings goals, even if it's just a small amount toward each.

No. This is a critical misconception. A charge-off is an internal accounting term for the creditor. The debt is still legally owed by you. The creditor can still pursue collection, sell the debt to a collection agency, or sue you for the balance.