The journey to becoming debt-free often feels less like a sprint and more like a meticulous archaeological dig, requiring one to carefully sift through the layers of their everyday financial life to uncover hidden resources. Finding extra money in your budget for debt repayment is not typically about a single windfall, but rather a conscious and sustained effort to align your spending with your priorities. It begins with a shift in perspective, viewing your budget not as a rigid constraint, but as a dynamic tool you control. The process hinges on three interconnected principles: rigorous examination, strategic reduction, and creative augmentation.The foundational step is to conduct a forensic audit of your current spending. This requires moving beyond broad categories and engaging in a granular, transaction-by-transaction review of the past two to three months. Every coffee, subscription box, and impulse buy must be accounted for. This exercise is often illuminating, revealing patterns of “leakage”—small, habitual expenditures that collectively form a significant monthly outflow. That daily gourmet coffee, the multiple streaming services you rarely use, and the premium cable package can silently drain hundreds of dollars annually. The goal here is not judgment but awareness. You cannot redirect money you do not know you are spending. This detailed ledger becomes the map that shows you exactly where your money is going, allowing you to make informed decisions rather than guesses.With clarity comes the power to strategically reduce expenses. This phase is about distinguishing between needs and wants and making intentional choices. Scrutinize your fixed expenses, which are often seen as immovable. Can you refinance your auto loan for a lower rate? Could you shop for cheaper insurance or bundle policies for a discount? Even a modest reduction in your monthly car insurance premium represents found money. For variable costs, embrace the power of substitution and moderation. Preparing meals at home rather than ordering takeout, utilizing public libraries for free entertainment, and implementing a 24-hour “cooling-off” period for non-essential purchases are all effective tactics. The objective is to create a sustainable, leaner lifestyle that temporarily prioritizes debt freedom without fostering resentment. This is not about deprivation, but about reallocating resources from less important areas to a critically important financial goal.Finally, look beyond mere reduction to creatively augment your income. Your budget has two sides: what goes out and what comes in. While cutting expenses has a limit, increasing your income offers a powerful accelerator for your debt repayment plan. Consider monetizing a skill or hobby in your spare time, such as freelance writing, graphic design, pet sitting, or tutoring. The digital economy offers platforms for selling handmade goods or even decluttering your home. A temporary part-time job, even for a few months, can generate a substantial debt-snowball payment. Any windfalls, like tax refunds, work bonuses, or cash gifts, should be directed immediately toward your debt principal. This proactive approach to boosting your cash inflows can dramatically shorten your debt timeline and reinforce your sense of agency.Ultimately, finding extra money for debt is an exercise in mindfulness and intentionality. It requires honest reflection, disciplined action, and a willingness to temporarily reshape your financial habits. By meticulously tracking your spending, strategically trimming the fat, and seeking opportunities to enhance your income, you systematically uncover the funds needed to attack your debt. The money is often already within your financial ecosystem, waiting to be redirected toward building a more secure and liberated future, free from the weight of financial obligations. The path to debt freedom is paved with the small, consistent decisions you make each day, transforming your budget from a record of expenses into a blueprint for financial liberation.

The journey to becoming debt-free often feels less like a sprint and more like a meticulous archaeological dig, requiring one to carefully sift through the layers of their everyday financial life to uncover hidden resources. Finding extra money in your budget for debt repayment is not typically about a single windfall, but rather a conscious and sustained effort to align your spending with your priorities. It begins with a shift in perspective, viewing your budget not as a rigid constraint, but as a dynamic tool you control. The process hinges on three interconnected principles: rigorous examination, strategic reduction, and creative augmentation.The foundational step is to conduct a forensic audit of your current spending. This requires moving beyond broad categories and engaging in a granular, transaction-by-transaction review of the past two to three months. Every coffee, subscription box, and impulse buy must be accounted for. This exercise is often illuminating, revealing patterns of “leakage”—small, habitual expenditures that collectively form a significant monthly outflow. That daily gourmet coffee, the multiple streaming services you rarely use, and the premium cable package can silently drain hundreds of dollars annually. The goal here is not judgment but awareness. You cannot redirect money you do not know you are spending. This detailed ledger becomes the map that shows you exactly where your money is going, allowing you to make informed decisions rather than guesses.With clarity comes the power to strategically reduce expenses. This phase is about distinguishing between needs and wants and making intentional choices. Scrutinize your fixed expenses, which are often seen as immovable. Can you refinance your auto loan for a lower rate? Could you shop for cheaper insurance or bundle policies for a discount? Even a modest reduction in your monthly car insurance premium represents found money. For variable costs, embrace the power of substitution and moderation. Preparing meals at home rather than ordering takeout, utilizing public libraries for free entertainment, and implementing a 24-hour “cooling-off” period for non-essential purchases are all effective tactics. The objective is to create a sustainable, leaner lifestyle that temporarily prioritizes debt freedom without fostering resentment. This is not about deprivation, but about reallocating resources from less important areas to a critically important financial goal.Finally, look beyond mere reduction to creatively augment your income. Your budget has two sides: what goes out and what comes in. While cutting expenses has a limit, increasing your income offers a powerful accelerator for your debt repayment plan. Consider monetizing a skill or hobby in your spare time, such as freelance writing, graphic design, pet sitting, or tutoring. The digital economy offers platforms for selling handmade goods or even decluttering your home. A temporary part-time job, even for a few months, can generate a substantial debt-snowball payment. Any windfalls, like tax refunds, work bonuses, or cash gifts, should be directed immediately toward your debt principal. This proactive approach to boosting your cash inflows can dramatically shorten your debt timeline and reinforce your sense of agency.Ultimately, finding extra money for debt is an exercise in mindfulness and intentionality. It requires honest reflection, disciplined action, and a willingness to temporarily reshape your financial habits. By meticulously tracking your spending, strategically trimming the fat, and seeking opportunities to enhance your income, you systematically uncover the funds needed to attack your debt. The money is often already within your financial ecosystem, waiting to be redirected toward building a more secure and liberated future, free from the weight of financial obligations. The path to debt freedom is paved with the small, consistent decisions you make each day, transforming your budget from a record of expenses into a blueprint for financial liberation.

By seeking free resources from reputable sources like non-profit credit counseling agencies, government websites (e.g., FTC, CFPB), libraries, and online financial education platforms.

Consult a non-profit credit counselor for a annual financial check-up, even if you feel fine. They can help you optimize your budget, identify potential risks, and provide strategies to stay on track before any trouble begins.

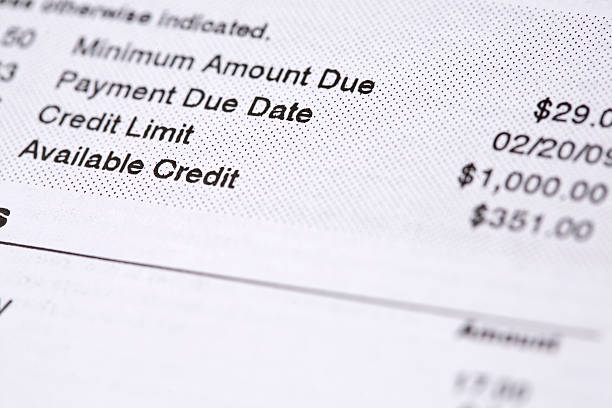

The debt-to-limit ratio, more commonly known as your credit utilization ratio, is the percentage of your available revolving credit (like credit cards) that you are currently using. It is calculated by dividing your total credit card balances by your total credit limits and multiplying by 100.

Yes, but providers typically require multiple notices and must follow state regulations. Shut-offs are often a last resort, especially for essential services like electricity or water.

Ceasing payments will lead to late fees, increased interest rates, and aggressive collection efforts, including lawsuits and potential wage garnishment. Creditors are not obligated to negotiate, and this strategy can significantly increase the total amount owed due to penalties.