Discovering an error related to old debt on your credit report can feel like confronting a ghost from your financial past. These inaccuracies, whether they involve debts that are past the statute of limitations, were already paid, or simply do not belong to you, can unjustly lower your credit score and hinder your ability to secure loans, housing, or employment. The process of disputing these errors is a right granted by the Fair Credit Reporting Act, and while it requires patience and diligence, it is a straightforward path to reclaiming your financial accuracy.The journey begins with obtaining your current credit reports. You are entitled to a free report from each of the three nationwide credit bureaus—Equifax, Experian, and TransUnion—every week through AnnualCreditReport.com. Once you have your reports, scrutinize each one carefully, as information can differ between bureaus. Identify the specific entry for the old debt, noting the creditor’s name, the account number, the reported balance, the date of first delinquency, and any status fields marked as “charged-off” or “in collections.“ This information will form the foundation of your dispute. It is also wise to gather any supporting documents you may have, such as old payment receipts, settlement letters, or bank statements, as these can be powerful evidence.With the error identified, the next step is to formally initiate the dispute. The most effective method is to send a detailed dispute letter by certified mail with a return receipt requested to the credit bureau that is reporting the inaccurate information. This creates a paper trail and proof of receipt. Your letter should clearly state your personal information, identify the inaccurate item by listing all the incorrect details, and concisely explain why the information is wrong—for instance, “This debt is past the seven-year reporting period,“ or “I settled this account in full on [date].“ Enclose copies of your supporting documents and a copy of your credit report with the item circled. Never send original documents. The credit bureau is legally obligated to investigate your claim, typically within thirty days, by contacting the data furnisher, which is the company that provided the old debt information.Simultaneously, it is a strategic move to send a similar dispute letter directly to the creditor or collection agency that furnished the erroneous information. This dual approach can often resolve the issue more quickly, as the furnisher must also investigate and report its findings back to the credit bureau. If the old debt is being reported by a collection agency, your dispute letter to them should reiterate the inaccuracy and demand validation of the debt, which is a separate right under the Fair Debt Collection Practices Act. If the information is indeed found to be incorrect or cannot be verified, both the furnisher and the credit bureau must correct or delete it.Following your dispute, the credit bureau will send you the results of its investigation in writing and a free copy of your report if the dispute resulted in a change. If your dispute is successful and the error is corrected, the negative item should be removed, potentially giving your credit score a welcome boost. However, if the investigation upholds the old debt as accurate and you still believe it to be wrong, you have the right to add a brief statement of dispute to your file, explaining your side of the story. For particularly stubborn or complex cases, especially those involving significant legal nuances around the age of the debt, seeking guidance from a non-profit credit counseling agency or a consumer law attorney specializing in credit reporting can be a prudent step.Ultimately, vigilance is your greatest ally in maintaining an accurate credit history. Old debts can sometimes resurface or be reported incorrectly due to administrative errors or when accounts are sold between collectors. By understanding your rights, methodically gathering evidence, and formally engaging with both the credit bureaus and data furnishers through written disputes, you can effectively challenge these lingering inaccuracies. This process not only cleans your financial slate but also reinforces the principle that your credit report should be a faithful reflection of your financial responsibilities, unburdened by the errors of the past.

Discovering an error related to old debt on your credit report can feel like confronting a ghost from your financial past. These inaccuracies, whether they involve debts that are past the statute of limitations, were already paid, or simply do not belong to you, can unjustly lower your credit score and hinder your ability to secure loans, housing, or employment. The process of disputing these errors is a right granted by the Fair Credit Reporting Act, and while it requires patience and diligence, it is a straightforward path to reclaiming your financial accuracy.The journey begins with obtaining your current credit reports. You are entitled to a free report from each of the three nationwide credit bureaus—Equifax, Experian, and TransUnion—every week through AnnualCreditReport.com. Once you have your reports, scrutinize each one carefully, as information can differ between bureaus. Identify the specific entry for the old debt, noting the creditor’s name, the account number, the reported balance, the date of first delinquency, and any status fields marked as “charged-off” or “in collections.“ This information will form the foundation of your dispute. It is also wise to gather any supporting documents you may have, such as old payment receipts, settlement letters, or bank statements, as these can be powerful evidence.With the error identified, the next step is to formally initiate the dispute. The most effective method is to send a detailed dispute letter by certified mail with a return receipt requested to the credit bureau that is reporting the inaccurate information. This creates a paper trail and proof of receipt. Your letter should clearly state your personal information, identify the inaccurate item by listing all the incorrect details, and concisely explain why the information is wrong—for instance, “This debt is past the seven-year reporting period,“ or “I settled this account in full on [date].“ Enclose copies of your supporting documents and a copy of your credit report with the item circled. Never send original documents. The credit bureau is legally obligated to investigate your claim, typically within thirty days, by contacting the data furnisher, which is the company that provided the old debt information.Simultaneously, it is a strategic move to send a similar dispute letter directly to the creditor or collection agency that furnished the erroneous information. This dual approach can often resolve the issue more quickly, as the furnisher must also investigate and report its findings back to the credit bureau. If the old debt is being reported by a collection agency, your dispute letter to them should reiterate the inaccuracy and demand validation of the debt, which is a separate right under the Fair Debt Collection Practices Act. If the information is indeed found to be incorrect or cannot be verified, both the furnisher and the credit bureau must correct or delete it.Following your dispute, the credit bureau will send you the results of its investigation in writing and a free copy of your report if the dispute resulted in a change. If your dispute is successful and the error is corrected, the negative item should be removed, potentially giving your credit score a welcome boost. However, if the investigation upholds the old debt as accurate and you still believe it to be wrong, you have the right to add a brief statement of dispute to your file, explaining your side of the story. For particularly stubborn or complex cases, especially those involving significant legal nuances around the age of the debt, seeking guidance from a non-profit credit counseling agency or a consumer law attorney specializing in credit reporting can be a prudent step.Ultimately, vigilance is your greatest ally in maintaining an accurate credit history. Old debts can sometimes resurface or be reported incorrectly due to administrative errors or when accounts are sold between collectors. By understanding your rights, methodically gathering evidence, and formally engaging with both the credit bureaus and data furnishers through written disputes, you can effectively challenge these lingering inaccuracies. This process not only cleans your financial slate but also reinforces the principle that your credit report should be a faithful reflection of your financial responsibilities, unburdened by the errors of the past.

While personal loans can lower interest rates, they often require good credit. If used without addressing spending habits, borrowers may end up with both a new loan and new credit card debt, worsening overextension.

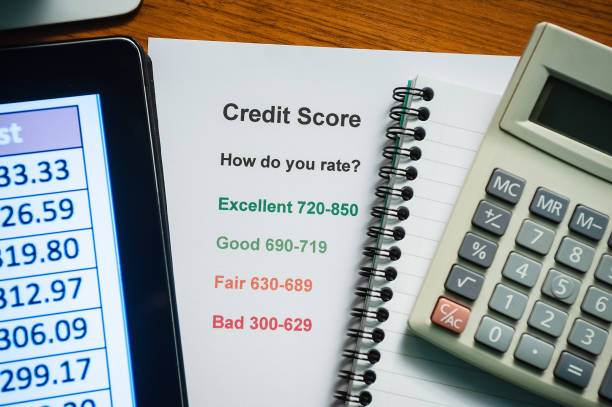

Your credit report is the detailed history of your credit accounts, payments, and inquiries. Your credit score is a three-digit number calculated from the information in your report. You have many scores, but you only have three main reports.

Read all terms carefully, especially fees, penalties, and APR changes. Avoid tools that encourage additional borrowing or seem too good to be true. Always have a repayment plan in place before using any credit product.

Settling may show as "settled" instead of "paid in full," which can still be viewed negatively. However, it prevents further damage from ongoing non-payment.

Leaving joint accounts open risks new charges by an ex-spouse, increasing your liability. Converting joint accounts to individual ones protects your credit and prevents further shared debt accumulation.