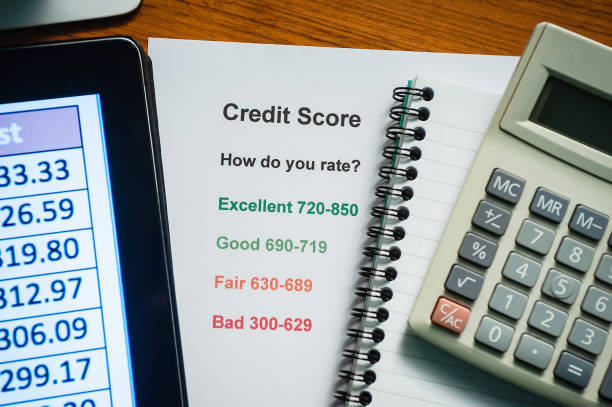

If you are struggling with credit card bills, a for-profit debt relief company can seem like a lifeline. You see the ads online. They promise to cut your debt in half. They claim they can stop the harassing phone calls from collectors. For a middle-class family trying to hold it together, that promise is hard to resist. The problem is that many of these companies are not designed to help you. They are designed to take your money while your credit score tanks and your debt gets worse.The most common and dangerous product sold by for-profit debt relief companies is something called a debt management plan or a debt settlement program. The pitch is simple. You stop paying your credit card bills directly. Instead, you send one monthly payment to the debt relief company. They put that money into a special account. They tell you to wait. Eventually, they say, they will negotiate with your creditors to settle your debts for a fraction of what you owe. It sounds neat and logical. In reality, it rarely works the way the salesperson described on the phone.The first problem is fees. For-profit debt relief companies are expensive. They often charge a percentage of your total debt, which can be fifteen to twenty-five percent of what you owe. On a ten thousand dollar credit card balance, that is up to twenty five hundred dollars just in fees. And they take that fee from the very first payments you send them. So while you think you are saving money for a settlement, a big chunk of your hard earned cash is going straight to the company that promised to save you.The second problem is time. These plans usually take three to four years to complete. During that entire time, you are not paying your credit card bills. Your creditors do not just sit around and wait politely. They charge late fees. They charge penalty interest rates that can hit thirty percent or more. They report your missed payments to the credit bureaus every single month. Within a few months, your credit score can drop by one hundred points or more. You might not care about your score when you are drowning in debt, but a low score makes it impossible to refinance your house, get a car loan, or even rent an apartment.Here is the part the salespeople do not mention. The creditors do not have to agree to a settlement. Many credit card companies will refuse to negotiate with a for-profit debt relief company at all. They will simply sue you for the full amount you owe. If they get a court judgment against you, they can garnish your wages or freeze your bank account. At that point, the money sitting in your debt relief account is not enough to cover what you owe, and you have nothing to show for the fees you already paid.The worst piece of this arrangement is the tax bomb. When a creditor agrees to settle a debt for less than you owe, the amount that is forgiven is considered taxable income by the IRS. If you settle a ten thousand dollar debt for five thousand dollars, you get a tax form showing five thousand dollars of income. Unless you have saved extra money to pay the tax bill, you end up owing the government on top of everything else. The debt relief company does not warn you about this because it hurts their sales pitch.There is a better path, but it is not the one advertised on late night television. Nonprofit credit counseling agencies, which are certified by organizations like the National Foundation for Credit Counseling, offer a different kind of help. They do not charge big upfront fees. They do not tell you to stop paying your bills. Instead, they work with your creditors to get the interest rates lowered and the late fees waived. You still pay back your full debt, but you do it over a longer period at a lower cost. Your credit score takes a hit because the accounts are marked as being on a payment plan, but it is nowhere near the damage caused by months of missed payments.Middle-class consumers need to understand one hard truth. If a company promises to get you out of debt easily or quickly, they are probably lying. Legitimate debt management is boring and slow. It requires discipline and patience. The for-profit companies know this, which is why they sell you a fantasy instead.Before you sign anything, ask the company one simple question. Are you a for-profit business? If the answer is yes, hang up the phone. Your money is better spent on a reputable nonprofit counselor who will actually put your interests first. Protecting your credit and your financial future starts with distrusting anyone who promises a shortcut.

If you are struggling with credit card bills, a for-profit debt relief company can seem like a lifeline. You see the ads online. They promise to cut your debt in half. They claim they can stop the harassing phone calls from collectors. For a middle-class family trying to hold it together, that promise is hard to resist. The problem is that many of these companies are not designed to help you. They are designed to take your money while your credit score tanks and your debt gets worse.The most common and dangerous product sold by for-profit debt relief companies is something called a debt management plan or a debt settlement program. The pitch is simple. You stop paying your credit card bills directly. Instead, you send one monthly payment to the debt relief company. They put that money into a special account. They tell you to wait. Eventually, they say, they will negotiate with your creditors to settle your debts for a fraction of what you owe. It sounds neat and logical. In reality, it rarely works the way the salesperson described on the phone.The first problem is fees. For-profit debt relief companies are expensive. They often charge a percentage of your total debt, which can be fifteen to twenty-five percent of what you owe. On a ten thousand dollar credit card balance, that is up to twenty five hundred dollars just in fees. And they take that fee from the very first payments you send them. So while you think you are saving money for a settlement, a big chunk of your hard earned cash is going straight to the company that promised to save you.The second problem is time. These plans usually take three to four years to complete. During that entire time, you are not paying your credit card bills. Your creditors do not just sit around and wait politely. They charge late fees. They charge penalty interest rates that can hit thirty percent or more. They report your missed payments to the credit bureaus every single month. Within a few months, your credit score can drop by one hundred points or more. You might not care about your score when you are drowning in debt, but a low score makes it impossible to refinance your house, get a car loan, or even rent an apartment.Here is the part the salespeople do not mention. The creditors do not have to agree to a settlement. Many credit card companies will refuse to negotiate with a for-profit debt relief company at all. They will simply sue you for the full amount you owe. If they get a court judgment against you, they can garnish your wages or freeze your bank account. At that point, the money sitting in your debt relief account is not enough to cover what you owe, and you have nothing to show for the fees you already paid.The worst piece of this arrangement is the tax bomb. When a creditor agrees to settle a debt for less than you owe, the amount that is forgiven is considered taxable income by the IRS. If you settle a ten thousand dollar debt for five thousand dollars, you get a tax form showing five thousand dollars of income. Unless you have saved extra money to pay the tax bill, you end up owing the government on top of everything else. The debt relief company does not warn you about this because it hurts their sales pitch.There is a better path, but it is not the one advertised on late night television. Nonprofit credit counseling agencies, which are certified by organizations like the National Foundation for Credit Counseling, offer a different kind of help. They do not charge big upfront fees. They do not tell you to stop paying your bills. Instead, they work with your creditors to get the interest rates lowered and the late fees waived. You still pay back your full debt, but you do it over a longer period at a lower cost. Your credit score takes a hit because the accounts are marked as being on a payment plan, but it is nowhere near the damage caused by months of missed payments.Middle-class consumers need to understand one hard truth. If a company promises to get you out of debt easily or quickly, they are probably lying. Legitimate debt management is boring and slow. It requires discipline and patience. The for-profit companies know this, which is why they sell you a fantasy instead.Before you sign anything, ask the company one simple question. Are you a for-profit business? If the answer is yes, hang up the phone. Your money is better spent on a reputable nonprofit counselor who will actually put your interests first. Protecting your credit and your financial future starts with distrusting anyone who promises a shortcut.

Once your DMP is accepted by your creditors and you begin making payments, most creditors will stop collection calls and waive late fees. This provides significant relief from collection harassment.

While a car loan is a liability that must be included, the car's current market value is an asset. This provides a true picture. For many, their car may be their largest physical asset, even as it depreciates.

Lenders may offer three loan options: a short-term with high payment, a long-term with a very high total cost, and a "decoy" option in the middle. The decoy makes the expensive long-term loan appear more reasonable by comparison, steering borrowers toward the most profitable option for the lender.

Federal law prohibits employers from firing an employee due to a single wage garnishment. However, if you have multiple garnishments, some state laws may allow termination.

The primary purpose is to create a clear, realistic plan that allocates your income toward essential expenses, debt repayment, and savings, ensuring you can meet your obligations while systematically reducing your debt over time.