If you fall behind on a debt and ignore the problem long enough, your creditor may decide to take a more aggressive approach than just calling or sending letters. One of the most powerful tools a creditor has is wage garnishment. This is a legal process that allows a creditor to take a portion of your paycheck directly from your employer before you ever see the money. For a middle-class consumer, wage garnishment can feel like a shock—and it can make an already tight budget even harder to manage.Wage garnishment does not happen overnight. First, you have to owe a debt and stop making payments. The creditor, whether it is a credit card company, a medical provider, or a personal loan lender, will usually try to collect on its own for several months. If that fails, they may sell the debt to a collection agency or hire a lawyer. Eventually, the creditor can sue you in court. If you do not respond to the lawsuit or show up in court, the judge will likely issue a default judgment in favor of the creditor. That judgment gives the creditor the legal right to collect the money by force.Once the creditor has a court judgment, they can ask the court for a writ of garnishment. This document is sent to your employer. Your employer is legally required to withhold a certain amount from each paycheck and send it directly to the creditor or the court. This continues until the debt is paid off or until you make other arrangements. Your employer cannot refuse unless they have a very good reason, and they may charge you a small administrative fee for processing the garnishment.The law protects some of your income. Under federal law, a creditor can take the lesser of two amounts: 25 percent of your disposable earnings, or the amount by which your weekly disposable earnings exceed 30 times the federal minimum wage. Disposable earnings are what is left after legally required deductions like taxes and Social Security. So if you earn $600 per week after taxes, 25 percent is $150. But 30 times the federal minimum wage ($7.25) equals $217.50. Your weekly disposable earnings of $600 exceed that by $382.50. The smaller number is $150, so that is what could be garnished. Some states have stricter limits, often 15 or 20 percent. Check your state laws, because they override the federal limit if they are more protective.Not all debts can be handled through wage garnishment. Child support, alimony, and unpaid taxes have their own rules and often take priority over regular consumer debts. Student loans in default can also trigger garnishment without a court judgment, as can federal taxes. But for credit cards, personal loans, medical bills, and most other unsecured debts, the creditor must first go through the lawsuit process.Wage garnishment hurts your credit score indirectly. The underlying lawsuit and judgment become public record and appear on your credit report. Judgments can stay on your credit report for seven years and significantly lower your score. Even if the garnishment itself does not show up as a separate line item, the fact that you have a judgment and missed payments will damage your credit. This makes it harder to get a mortgage, car loan, or even rent an apartment.If your wages are being garnished, you do have options. The most important thing is to act quickly. You can try to negotiate a lump-sum settlement with the creditor to stop the garnishment. Sometimes they will accept a lower amount to get paid faster. You can also ask the court to reduce the amount based on financial hardship. If you can prove that the garnishment leaves you unable to cover basic living expenses, a judge may lower the percentage. Filing for bankruptcy is a more drastic step, but it will stop most garnishments immediately and can discharge the debt entirely. Chapter 7 bankruptcy can wipe out unsecured debts, while Chapter 13 sets up a repayment plan that stops garnishments.Your employer is not allowed to fire you because of a single wage garnishment. The federal Consumer Credit Protection Act prohibits termination for one garnishment. However, if your wages are garnished for two or more separate debts, your employer may be allowed to let you go. That is one more reason to deal with the problem before it multiplies.The best way to avoid wage garnishment is to face your debt early. If you are having trouble making payments, call your creditor and explain your situation. Many will work with you on a reduced payment plan or allow a temporary deferment. If you are already being sued, do not ignore the court summons. Show up and explain your side. You may be able to negotiate a payment agreement before a judgment is entered. Once a judgment exists, the creditor can garnish wages, freeze your bank account, or place a lien on your property. Garnishment is often the most painful outcome because it directly reduces your income week after week.Understanding wage garnishment helps you take control of your finances. It is not something that happens by accident. It is the result of a legal process that starts with unpaid debt and ends with a court order. If you stay engaged with your creditors and respond quickly to any lawsuits, you can usually avoid garnishment altogether. If it does happen, know that you have legal rights, limits on what can be taken, and options to stop it. The key is to act, not to hide.

If you fall behind on a debt and ignore the problem long enough, your creditor may decide to take a more aggressive approach than just calling or sending letters. One of the most powerful tools a creditor has is wage garnishment. This is a legal process that allows a creditor to take a portion of your paycheck directly from your employer before you ever see the money. For a middle-class consumer, wage garnishment can feel like a shock—and it can make an already tight budget even harder to manage.Wage garnishment does not happen overnight. First, you have to owe a debt and stop making payments. The creditor, whether it is a credit card company, a medical provider, or a personal loan lender, will usually try to collect on its own for several months. If that fails, they may sell the debt to a collection agency or hire a lawyer. Eventually, the creditor can sue you in court. If you do not respond to the lawsuit or show up in court, the judge will likely issue a default judgment in favor of the creditor. That judgment gives the creditor the legal right to collect the money by force.Once the creditor has a court judgment, they can ask the court for a writ of garnishment. This document is sent to your employer. Your employer is legally required to withhold a certain amount from each paycheck and send it directly to the creditor or the court. This continues until the debt is paid off or until you make other arrangements. Your employer cannot refuse unless they have a very good reason, and they may charge you a small administrative fee for processing the garnishment.The law protects some of your income. Under federal law, a creditor can take the lesser of two amounts: 25 percent of your disposable earnings, or the amount by which your weekly disposable earnings exceed 30 times the federal minimum wage. Disposable earnings are what is left after legally required deductions like taxes and Social Security. So if you earn $600 per week after taxes, 25 percent is $150. But 30 times the federal minimum wage ($7.25) equals $217.50. Your weekly disposable earnings of $600 exceed that by $382.50. The smaller number is $150, so that is what could be garnished. Some states have stricter limits, often 15 or 20 percent. Check your state laws, because they override the federal limit if they are more protective.Not all debts can be handled through wage garnishment. Child support, alimony, and unpaid taxes have their own rules and often take priority over regular consumer debts. Student loans in default can also trigger garnishment without a court judgment, as can federal taxes. But for credit cards, personal loans, medical bills, and most other unsecured debts, the creditor must first go through the lawsuit process.Wage garnishment hurts your credit score indirectly. The underlying lawsuit and judgment become public record and appear on your credit report. Judgments can stay on your credit report for seven years and significantly lower your score. Even if the garnishment itself does not show up as a separate line item, the fact that you have a judgment and missed payments will damage your credit. This makes it harder to get a mortgage, car loan, or even rent an apartment.If your wages are being garnished, you do have options. The most important thing is to act quickly. You can try to negotiate a lump-sum settlement with the creditor to stop the garnishment. Sometimes they will accept a lower amount to get paid faster. You can also ask the court to reduce the amount based on financial hardship. If you can prove that the garnishment leaves you unable to cover basic living expenses, a judge may lower the percentage. Filing for bankruptcy is a more drastic step, but it will stop most garnishments immediately and can discharge the debt entirely. Chapter 7 bankruptcy can wipe out unsecured debts, while Chapter 13 sets up a repayment plan that stops garnishments.Your employer is not allowed to fire you because of a single wage garnishment. The federal Consumer Credit Protection Act prohibits termination for one garnishment. However, if your wages are garnished for two or more separate debts, your employer may be allowed to let you go. That is one more reason to deal with the problem before it multiplies.The best way to avoid wage garnishment is to face your debt early. If you are having trouble making payments, call your creditor and explain your situation. Many will work with you on a reduced payment plan or allow a temporary deferment. If you are already being sued, do not ignore the court summons. Show up and explain your side. You may be able to negotiate a payment agreement before a judgment is entered. Once a judgment exists, the creditor can garnish wages, freeze your bank account, or place a lien on your property. Garnishment is often the most painful outcome because it directly reduces your income week after week.Understanding wage garnishment helps you take control of your finances. It is not something that happens by accident. It is the result of a legal process that starts with unpaid debt and ends with a court order. If you stay engaged with your creditors and respond quickly to any lawsuits, you can usually avoid garnishment altogether. If it does happen, know that you have legal rights, limits on what can be taken, and options to stop it. The key is to act, not to hide.

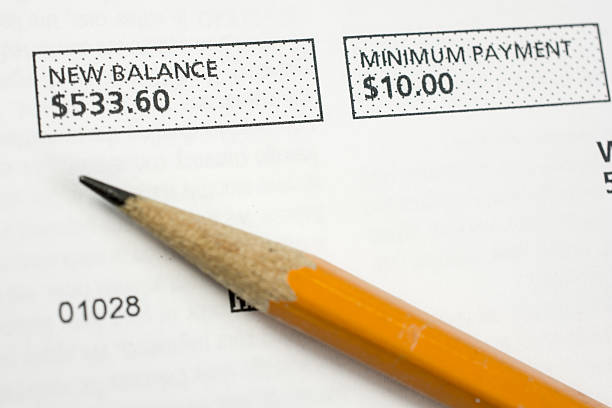

Making only minimum payments extends the repayment period drastically and maximizes interest costs. This keeps your debt balances high, maintains a high DTI, and traps you in a cycle where progress is slow and financial flexibility remains limited.

Tax debt owed to government agencies (e.g., IRS) cannot be discharged easily and may involve penalties, interest, and legal actions like wage garnishment or liens, making it particularly urgent and severe.

A bloated car payment consumes income that should go toward retirement savings, emergency funds, and other essential goals, crippling your ability to build long-term wealth and financial security.

Lenders see you as high-risk, resulting in much higher interest rates on any new credit you qualify for, such as auto loans or mortgages. This can cost you tens of thousands of dollars over the life of a loan.

You make minimum payments on all debts but focus any extra repayment funds on the debt with the smallest outstanding balance. After paying it off, you take the total amount you were paying on that debt and apply it to the next smallest balance.