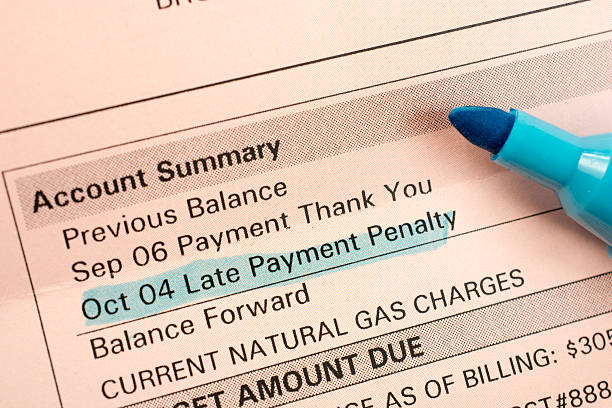

An introductory credit card offer feels like a breath of fresh air. Zero percent interest on purchases for 15 months, a teaser rate on balance transfers that gives you room to pay down debt, or even a low fixed rate for a set period. It is easy to get caught up in the promotional glow and forget that these rates are temporary. Once the music stops, the regular annual percentage rate, or APR, takes over, and that number will quietly shape what you actually pay for carrying a balance. Learning how to compare that regular APR across different cards is one of the most practical skills a middle-class household can build. It keeps you from trading a short-term break for long-term costs you did not see coming.The first step is to know exactly what you are looking at. When a credit card issuer advertises an introductory APR, they are promoting a temporary rate that applies to specific transactions. Those transactions might be new purchases, balance transfers, or in rare cases both. The introductory offer lasts for a defined number of months from account opening. After that window closes, any remaining balance shifts to the card’s regular APR. This is the ongoing rate that will apply for as long as you have the card, unless the issuer changes it with proper notice. That regular APR is what you need to compare, because unless you pay your balance in full before the promotional clock runs out, this is the number that will generate your interest charges month after month.You will find the regular APR clearly listed in the card’s pricing and terms, often inside a standardized table called the Schumer box. Look for phrases such as “ongoing APR,” “standard APR,” or “regular APR for purchases.” They usually show a range, like 17.99 percent to 28.24 percent, because the exact rate you receive depends on your creditworthiness at the time of application. The vast majority of cards today offer variable APRs, meaning the rate is tied to an index, generally the prime rate, plus a fixed margin set by the issuer. If the prime rate goes up, your regular APR will follow. So when you compare regular APRs, you are comparing both the margin and the current rate environment, understanding that the number can drift over time.To make a meaningful comparison, you need to line up the same type of APR from each card you are considering. Someone shopping for a card to finance a large purchase should focus on the regular purchase APR after the intro. Someone consolidating high-interest debt onto a balance transfer card should zero in on the regular balance transfer APR. These rates can be different even on the same card. A card might have a reasonable purchase APR but a much higher balance transfer APR once the promotional period ends. If you transfer a balance and do not wipe it out completely during the zero-rate window, the remaining amount will immediately begin accruing interest at that regular balance transfer rate, which could be steep. Comparing apples to apples ensures you see the true cost of any leftover balance.Think beyond the number itself. The difference between a regular APR of 18 percent and one of 25 percent might sound abstract until you translate it into dollars. Imagine you have a two-thousand-dollar balance lingering after an intro offer. At 18 percent, monthly interest is roughly thirty dollars, adding up to over three hundred fifty dollars if it takes a year to pay off. At 25 percent, that same balance costs about forty-two dollars a month and more than five hundred dollars over a year. That is money you could have used for a car repair, a child’s summer camp, or an extra payment on a mortgage. When you compare regular APRs, you are really comparing how much of your hard-earned cash will disappear into interest if life slows down your payoff plan.Another layer to watch for is the penalty APR. This is a sky-high rate, sometimes close to thirty percent, that kicks in if you make a late payment or violate other card terms. Not every card has one, but when it exists, it can permanently raise your regular APR on existing balances. As you compare offers, glance at the penalty APR disclosure and consider whether the risk makes one card more dangerous than another. A card with an otherwise competitive regular APR might be a poor choice if a single slip-up locks you into an even worse rate for months. The stability of the rate matters almost as much as the starting figure.Context makes comparisons clearer. If you are certain you can pay off a purchase or balance transfer before the introductory timer expires, the regular APR may seem irrelevant. Life, however, has a way of rewriting budgets. A job loss, a medical bill, or a pressing home expense can stretch that timeline. Giving extra weight to a lower regular APR acts as a safety net. A card with a nine-month zero-rate window and a 14 percent regular APR might serve you better over the long haul than a card offering eighteen months at zero percent but a 28 percent regular APR, especially if you suspect the balance will follow you past the party. Neither choice is inherently wrong, but the comparison lets you make an informed trade-off.When you sit down to compare, pull up the pricing information for each card and jot down three things: the regular purchase APR, the regular balance transfer APR, and whether a penalty rate exists. Then ask yourself which activity you are most likely to carry beyond the introductory period. Use that scenario to weigh the numbers. A card with a lower regular balance transfer APR might save you hundreds over one with an extra couple of months of zero interest. If you plan to treat the card as an everyday spending tool and occasionally float a balance, a reliably low purchase APR is gold. The key is to stop seeing the introductory offer as the main event and start treating the regular APR as the quiet partner that will stick around long after the balloons are gone.Comparing regular APRs does not require a finance degree or a magnifying glass. It simply asks you to read the straightforward disclosures that card issuers are required to provide and to think about what happens when the welcome mat disappears. By putting the regular rate at the center of your decision, you tilt the odds in your favor. You choose a card that works not just for the first few months, but for the everyday reality of your financial life. And in a world where a single percentage point can mean hundreds of dollars a year, that quiet discipline is a genuine form of wealth protection.

An introductory credit card offer feels like a breath of fresh air. Zero percent interest on purchases for 15 months, a teaser rate on balance transfers that gives you room to pay down debt, or even a low fixed rate for a set period. It is easy to get caught up in the promotional glow and forget that these rates are temporary. Once the music stops, the regular annual percentage rate, or APR, takes over, and that number will quietly shape what you actually pay for carrying a balance. Learning how to compare that regular APR across different cards is one of the most practical skills a middle-class household can build. It keeps you from trading a short-term break for long-term costs you did not see coming.The first step is to know exactly what you are looking at. When a credit card issuer advertises an introductory APR, they are promoting a temporary rate that applies to specific transactions. Those transactions might be new purchases, balance transfers, or in rare cases both. The introductory offer lasts for a defined number of months from account opening. After that window closes, any remaining balance shifts to the card’s regular APR. This is the ongoing rate that will apply for as long as you have the card, unless the issuer changes it with proper notice. That regular APR is what you need to compare, because unless you pay your balance in full before the promotional clock runs out, this is the number that will generate your interest charges month after month.You will find the regular APR clearly listed in the card’s pricing and terms, often inside a standardized table called the Schumer box. Look for phrases such as “ongoing APR,” “standard APR,” or “regular APR for purchases.” They usually show a range, like 17.99 percent to 28.24 percent, because the exact rate you receive depends on your creditworthiness at the time of application. The vast majority of cards today offer variable APRs, meaning the rate is tied to an index, generally the prime rate, plus a fixed margin set by the issuer. If the prime rate goes up, your regular APR will follow. So when you compare regular APRs, you are comparing both the margin and the current rate environment, understanding that the number can drift over time.To make a meaningful comparison, you need to line up the same type of APR from each card you are considering. Someone shopping for a card to finance a large purchase should focus on the regular purchase APR after the intro. Someone consolidating high-interest debt onto a balance transfer card should zero in on the regular balance transfer APR. These rates can be different even on the same card. A card might have a reasonable purchase APR but a much higher balance transfer APR once the promotional period ends. If you transfer a balance and do not wipe it out completely during the zero-rate window, the remaining amount will immediately begin accruing interest at that regular balance transfer rate, which could be steep. Comparing apples to apples ensures you see the true cost of any leftover balance.Think beyond the number itself. The difference between a regular APR of 18 percent and one of 25 percent might sound abstract until you translate it into dollars. Imagine you have a two-thousand-dollar balance lingering after an intro offer. At 18 percent, monthly interest is roughly thirty dollars, adding up to over three hundred fifty dollars if it takes a year to pay off. At 25 percent, that same balance costs about forty-two dollars a month and more than five hundred dollars over a year. That is money you could have used for a car repair, a child’s summer camp, or an extra payment on a mortgage. When you compare regular APRs, you are really comparing how much of your hard-earned cash will disappear into interest if life slows down your payoff plan.Another layer to watch for is the penalty APR. This is a sky-high rate, sometimes close to thirty percent, that kicks in if you make a late payment or violate other card terms. Not every card has one, but when it exists, it can permanently raise your regular APR on existing balances. As you compare offers, glance at the penalty APR disclosure and consider whether the risk makes one card more dangerous than another. A card with an otherwise competitive regular APR might be a poor choice if a single slip-up locks you into an even worse rate for months. The stability of the rate matters almost as much as the starting figure.Context makes comparisons clearer. If you are certain you can pay off a purchase or balance transfer before the introductory timer expires, the regular APR may seem irrelevant. Life, however, has a way of rewriting budgets. A job loss, a medical bill, or a pressing home expense can stretch that timeline. Giving extra weight to a lower regular APR acts as a safety net. A card with a nine-month zero-rate window and a 14 percent regular APR might serve you better over the long haul than a card offering eighteen months at zero percent but a 28 percent regular APR, especially if you suspect the balance will follow you past the party. Neither choice is inherently wrong, but the comparison lets you make an informed trade-off.When you sit down to compare, pull up the pricing information for each card and jot down three things: the regular purchase APR, the regular balance transfer APR, and whether a penalty rate exists. Then ask yourself which activity you are most likely to carry beyond the introductory period. Use that scenario to weigh the numbers. A card with a lower regular balance transfer APR might save you hundreds over one with an extra couple of months of zero interest. If you plan to treat the card as an everyday spending tool and occasionally float a balance, a reliably low purchase APR is gold. The key is to stop seeing the introductory offer as the main event and start treating the regular APR as the quiet partner that will stick around long after the balloons are gone.Comparing regular APRs does not require a finance degree or a magnifying glass. It simply asks you to read the straightforward disclosures that card issuers are required to provide and to think about what happens when the welcome mat disappears. By putting the regular rate at the center of your decision, you tilt the odds in your favor. You choose a card that works not just for the first few months, but for the everyday reality of your financial life. And in a world where a single percentage point can mean hundreds of dollars a year, that quiet discipline is a genuine form of wealth protection.

Your 40s are peak earning years and your last major window to build retirement wealth. Debt payments directly sabotage your ability to save, jeopardizing your entire retirement plan and leaving insufficient time to recover.

Individuals may not know methods like the debt avalanche (paying high-interest debt first) or snowball (paying small balances first) methods, so they pay debts inefficiently, costing more time and money.

Yes. Many hospitals offer financial assistance programs (charity care) based on income. Nonprofits like RIP Medical Debt也可能 help eliminate debts for eligible individuals.

A balance transfer card can be useful if you have high-interest credit card debt and can qualify for a card with a low or 0% introductory APR. This allows you to save on interest and pay down principal faster, but requires discipline to pay off the balance before the promotional period ends.

Focus on building a budget, establishing an emergency fund, and aggressively tackling high-interest credit card debt first. Take advantage of longer time horizons to recover and build positive financial habits.