If you fall behind on a debt long enough, your creditor may decide to take more aggressive action to get their money. One of the most serious steps they can take is called wage garnishment. This is when a court orders your employer to take a portion of your paycheck and send it directly to the creditor until the debt is paid off. It is not something that happens overnight, but it is a real possibility if you ignore collection calls or stop making payments entirely. Understanding how wage garnishment works can help you protect your income and avoid a financial shock.First, it is important to know that a creditor cannot just decide to garnish your wages on their own. They must first sue you in court and win a judgment against you. If you never respond to the lawsuit, the court will likely issue a default judgment, which means the creditor automatically wins because you did not show up. Once they have that judgment, they can ask the court for a wage garnishment order. Typically, this order is sent to your employer, who is legally required to follow it. Your employer cannot fire you because of one garnishment, but they can face penalties if they ignore the order.How much can be taken from your paycheck depends on federal law and the laws of your state. Federal law says that the amount garnished cannot exceed 25 percent of your disposable earnings, or the amount by which your weekly income exceeds thirty times the federal minimum wage, whichever is lower. Some states have even stricter limits. For example, in Texas, wage garnishment is generally not allowed for consumer debts, but it is allowed for child support, student loans, and taxes. In other states, the cap might be 15 percent. This means that even if you owe a large amount, the creditor can only take a little bit at a time, which can make repayment very slow.The process is not immediate. After the court issues the garnishment order, your employer will receive a document called a writ of garnishment. They will then calculate the amount to withhold from your paycheck each pay period and send it to the court or directly to the creditor. This can go on for months or even years until the debt is fully paid. Meanwhile, you still have to pay your regular bills, rent, and groceries. Losing even a quarter of your take-home pay can be devastating for a middle-class family that is already stretched thin.What types of debts lead to wage garnishment? The most common are credit card debt, personal loans, medical bills, and auto loans after the car has been repossessed if there is still a balance. Government debts like student loans and back taxes have much stronger collection powers. For federal student loans, the government can garnish your wages without first getting a court order. This is called administrative garnishment, and it has its own limits. Generally, they can take up to 15 percent of your disposable income. For back taxes, the IRS can levy your wages, which is similar to garnishment but even more aggressive.If you are facing wage garnishment, you have some options. You can try to negotiate with the creditor to settle the debt for a lower amount. Many creditors would rather get a lump sum payment than go through the slow garnishment process. You can also file for bankruptcy, which immediately stops all garnishments through an automatic stay. However, bankruptcy is a serious step that affects your credit for years. Another option is to ask the court for a hardship exemption. If you can prove that garnishment would prevent you from paying for basic necessities like food, housing, or medical care, the court may reduce the amount or stop the garnishment entirely. This is not guaranteed, but it is worth trying if you are truly struggling.The emotional impact of wage garnishment should not be overlooked. It can be embarrassing to have your employer know about your debt problems. It can also cause tension at work if your payroll department has to send your paycheck to a court instead of to you. Some people try to quit their job to avoid garnishment, but that only makes things worse because you will lose income entirely and the garnishment order can follow you to a new job. It is better to stay employed and find a way to manage the situation.The best defense against wage garnishment is to stay in communication with your creditors before they sue you. If you are having trouble paying, call them and explain your situation. Many creditors will work out a payment plan or offer a temporary reduction. Ignoring the problem only makes it more likely that they will file a lawsuit and eventually garnish your wages. Also, keep your address current with creditors so you do not miss a court summons. If you are served with a lawsuit, do not ignore it. Even if you cannot pay the full amount, showing up in court gives you the chance to negotiate a settlement or argue that the debt is not valid.Wage garnishment is a powerful tool for creditors, but it is not unstoppable. By understanding your rights and taking action early, you can often avoid it altogether. If you are already in the middle of garnishment, focus on your budget, seek help from a credit counselor, and consider legal advice. The goal is to get the debt behind you without losing your ability to earn a living.

If you fall behind on a debt long enough, your creditor may decide to take more aggressive action to get their money. One of the most serious steps they can take is called wage garnishment. This is when a court orders your employer to take a portion of your paycheck and send it directly to the creditor until the debt is paid off. It is not something that happens overnight, but it is a real possibility if you ignore collection calls or stop making payments entirely. Understanding how wage garnishment works can help you protect your income and avoid a financial shock.First, it is important to know that a creditor cannot just decide to garnish your wages on their own. They must first sue you in court and win a judgment against you. If you never respond to the lawsuit, the court will likely issue a default judgment, which means the creditor automatically wins because you did not show up. Once they have that judgment, they can ask the court for a wage garnishment order. Typically, this order is sent to your employer, who is legally required to follow it. Your employer cannot fire you because of one garnishment, but they can face penalties if they ignore the order.How much can be taken from your paycheck depends on federal law and the laws of your state. Federal law says that the amount garnished cannot exceed 25 percent of your disposable earnings, or the amount by which your weekly income exceeds thirty times the federal minimum wage, whichever is lower. Some states have even stricter limits. For example, in Texas, wage garnishment is generally not allowed for consumer debts, but it is allowed for child support, student loans, and taxes. In other states, the cap might be 15 percent. This means that even if you owe a large amount, the creditor can only take a little bit at a time, which can make repayment very slow.The process is not immediate. After the court issues the garnishment order, your employer will receive a document called a writ of garnishment. They will then calculate the amount to withhold from your paycheck each pay period and send it to the court or directly to the creditor. This can go on for months or even years until the debt is fully paid. Meanwhile, you still have to pay your regular bills, rent, and groceries. Losing even a quarter of your take-home pay can be devastating for a middle-class family that is already stretched thin.What types of debts lead to wage garnishment? The most common are credit card debt, personal loans, medical bills, and auto loans after the car has been repossessed if there is still a balance. Government debts like student loans and back taxes have much stronger collection powers. For federal student loans, the government can garnish your wages without first getting a court order. This is called administrative garnishment, and it has its own limits. Generally, they can take up to 15 percent of your disposable income. For back taxes, the IRS can levy your wages, which is similar to garnishment but even more aggressive.If you are facing wage garnishment, you have some options. You can try to negotiate with the creditor to settle the debt for a lower amount. Many creditors would rather get a lump sum payment than go through the slow garnishment process. You can also file for bankruptcy, which immediately stops all garnishments through an automatic stay. However, bankruptcy is a serious step that affects your credit for years. Another option is to ask the court for a hardship exemption. If you can prove that garnishment would prevent you from paying for basic necessities like food, housing, or medical care, the court may reduce the amount or stop the garnishment entirely. This is not guaranteed, but it is worth trying if you are truly struggling.The emotional impact of wage garnishment should not be overlooked. It can be embarrassing to have your employer know about your debt problems. It can also cause tension at work if your payroll department has to send your paycheck to a court instead of to you. Some people try to quit their job to avoid garnishment, but that only makes things worse because you will lose income entirely and the garnishment order can follow you to a new job. It is better to stay employed and find a way to manage the situation.The best defense against wage garnishment is to stay in communication with your creditors before they sue you. If you are having trouble paying, call them and explain your situation. Many creditors will work out a payment plan or offer a temporary reduction. Ignoring the problem only makes it more likely that they will file a lawsuit and eventually garnish your wages. Also, keep your address current with creditors so you do not miss a court summons. If you are served with a lawsuit, do not ignore it. Even if you cannot pay the full amount, showing up in court gives you the chance to negotiate a settlement or argue that the debt is not valid.Wage garnishment is a powerful tool for creditors, but it is not unstoppable. By understanding your rights and taking action early, you can often avoid it altogether. If you are already in the middle of garnishment, focus on your budget, seek help from a credit counselor, and consider legal advice. The goal is to get the debt behind you without losing your ability to earn a living.

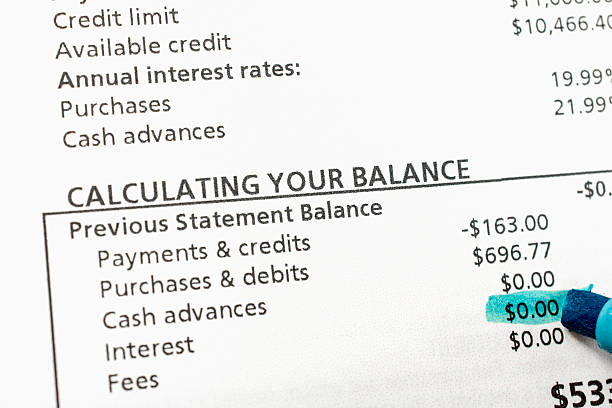

A cash advance allows you to withdraw cash from an ATM or bank using your credit card. It immediately accrues interest at a much higher APR than purchases, has no grace period, and often includes an additional transaction fee, making it an extremely expensive form of debt.

Non-profit organizations like the National Foundation for Credit Counseling (NFCC) offer certified financial counselors. For mental health, consider therapy, community health services, or support groups like Debtors Anonymous. The 988 Suicide & Crisis Lifeline is available for immediate crisis support.

The most problematic debts are often a combination of lingering student loans, large mortgages, expensive auto loans, and high-interest credit card debt accumulated from lifestyle inflation, child-rearing costs, or covering budget shortfalls.

This is a letter you can send to a collector demanding they prove you legally owe the debt and that they have the right to collect it. They must cease collection efforts until they provide this validation. This is a powerful tool to ensure the debt is legitimate.

Temporary gig work, freelance opportunities, or part-time jobs can generate immediate cash flow to help cover essential expenses while seeking more permanent employment.